The VIX, formerly the Chicago Board Options Exchange (CBOE) Volatility Index, often referred to as the “fear gauge,” serves as a valuable tool for options sellers like us. It captures market sentiment by rising with increased uncertainty and concern, as reflected by the weighted average of out-of-the-money call and put options on the S&P 500. Consequently, when option prices increase, the VIX climbs as well, providing insights into market volatility. This unique index forms the foundation for various investment and options trading strategies.

While the VIX itself isn’t directly tradable due to its unique structure, you can gain exposure through VIX futures and options on those futures. However, these instruments are complex and require careful consideration due to their various nuances. VIX futures contracts are tied to specific expiration dates and may differ significantly in value from the VIX index itself. This divergence stems from a concept known as the “term structure,” which typically manifests as contango. In contango, longer-dated futures contracts trade at a premium compared to near-term contracts.

Volatility Products

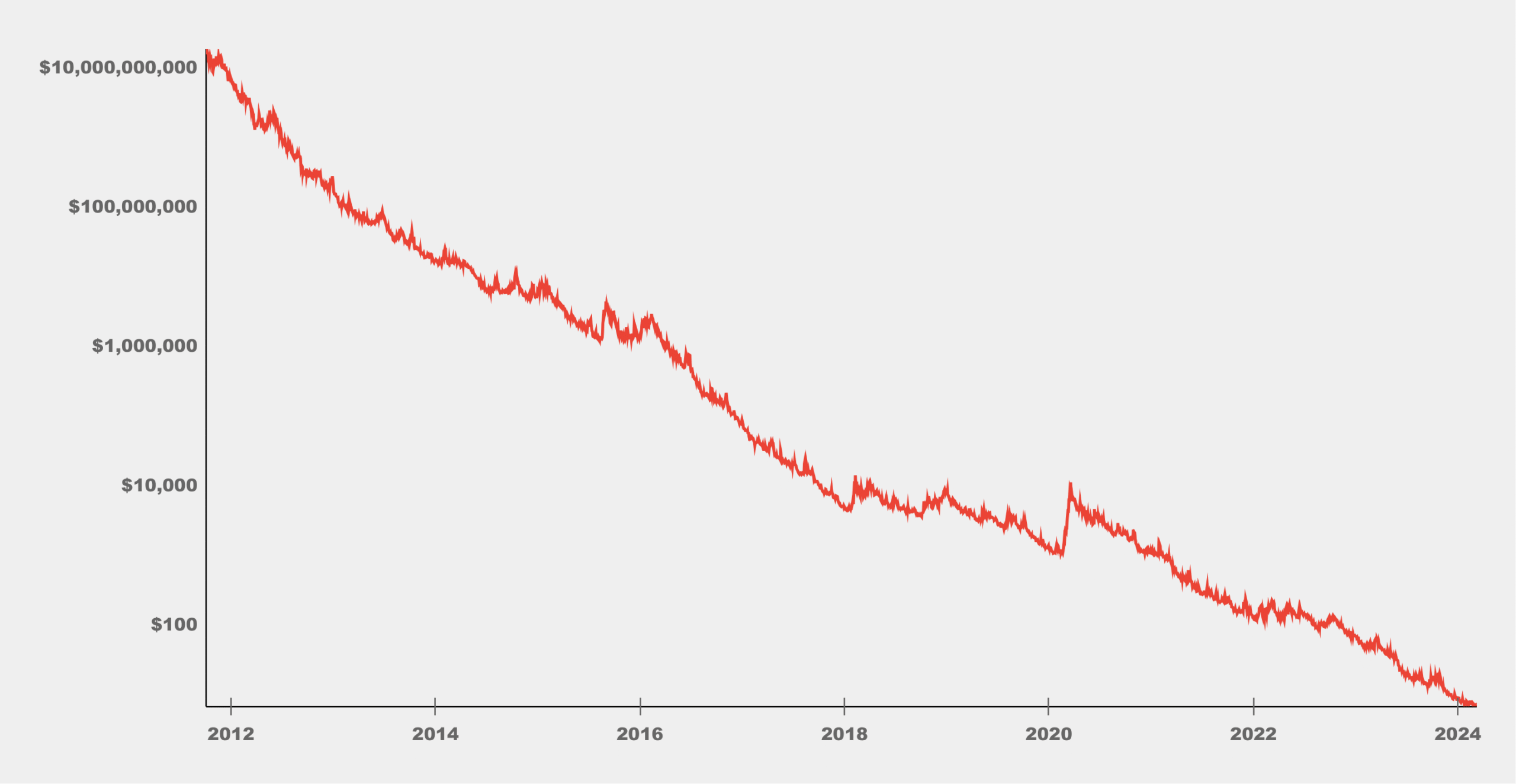

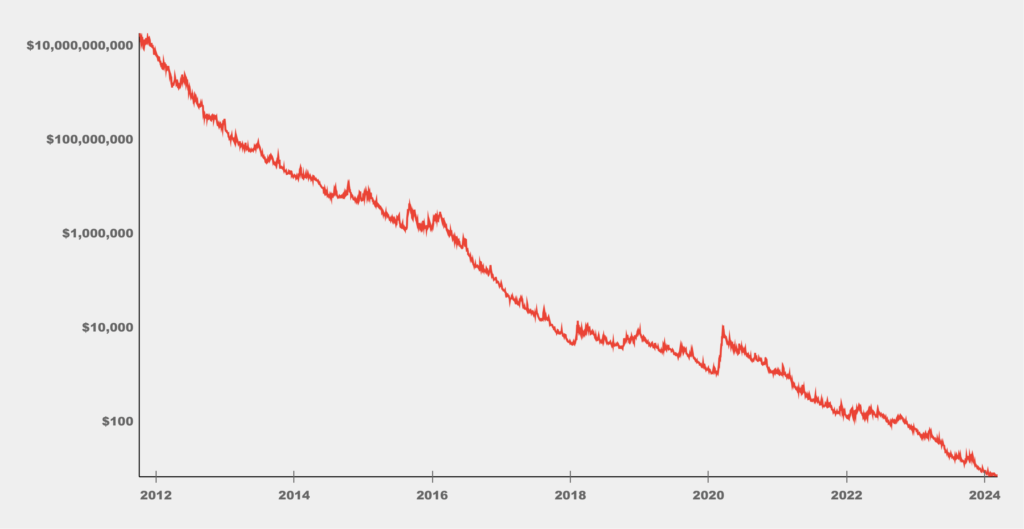

Another way to trade the VIX is with exchange-traded funds (ETFs) and exchange-traded notes (ETNs) based on VIX futures. As exchange-traded products, you can buy and sell these securities like stocks, simplifying your VIX trading strategy. The first and most well-known of these products is Barclays’ VXX, an ETN that tracks the VIX short-term futures. However, it has lost more than 99% of its value since its inception in 2009. This dramatic decline isn’t unique to VXX c other volatility products like the popular UVXY ETF, have also experienced similar erosion over time. This might leave you wondering: why do these products tracking the VIX experience such a significant loss, and will they eventually reach zero?

Volatility Decay

The culprit behind VXX’s dramatic value erosion is a concept I’ve mentioned earlier: contango. In futures markets, contracts expiring further out typically trade at a premium compared to those nearing expiry. This reflects the market’s expectation of higher volatility in the future. VXX tracks the rolling of the first- and second-month VIX futures to maintain a constant 30-day average maturity to avoid underlying product expiration risk. The problem? These front-month contracts constantly near expiry, forcing VXX to roll them into newer, typically more expensive futures contracts (with higher premiums due to contango). Over time, this continuous rolling erodes VXX’s value, leading to the significant decline.

To elaborate on the rebalancing process, let’s consider a hypothetical example. Imagine at market close today, VXX holds 86% of its portfolio in VIX futures expiring next month (front-month) and 14% in futures expiring in two months (back-month). At market close tomorrow, VXX will shift 4% of their holdings from next month’s (front-month) futures contracts into the futures contracts that expire in two months (back-month). After the rebalance, VXX’s holdings will consist of an 82% front-month weighting and an 18% back-month weighting. This rebalancing cycle continues indefinitely at the end market close each day. Once the front-month contract expires, 100% of the holdings will be in the back-month futures, which becomes the new front-month as the cycle restarts.

Due to its inherent price decay, VXX’s share price can gradually decline to very low levels, creating challenges for both options contracts tied to VXX and maintaining exchange listing requirements. Reverse splits are a necessary tool to address these issues by keeping the price within a reasonable trading range. Without reverse splits, VXX’s share price could rapidly approach zero. The first split for VXX occurred on November 9th, 2010. This was a 1 for 4 reverse split, meaning for each 4 shares of VXX owned before the split, shareholders ended up with 1 share after the split. On March 7th, 2023, VXX just made its seventh 1 for 4 stock split.

| Date | Price at split | Months since last split | Split ratio | |

| 1. | November 9th, 2010 | 13.11 | 21 (since inception) | 1 for 4 |

| 2. | October 5th, 2012 | 8.77 | 23 | 1 for 4 |

| 3. | November 8th, 2013 | 12.84 | 13 | 1 for 4 |

| 4. | August 9th, 2016 | 9.27 | 33 | 1 for 4 |

| 5. | August 23rd, 2017 | 11.94 | 13 | 1 for 4 |

| 6. | April 23rd, 2021 | 10.45 | 44 | 1 for 4 |

| 7. | March 7th, 2023 | 10.71 | 23 | 1 for 4 |

Is Shorting VXX the Perfect Trade?

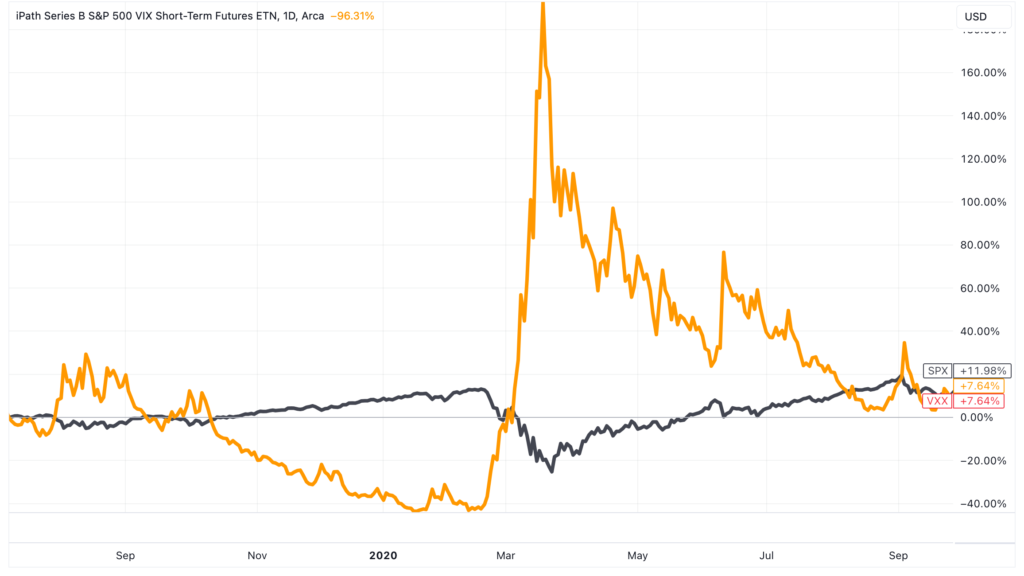

Looking at VXX’s historical price decay, it’s easy to wonder: why isn’t everyone shorting it? Wouldn’t selling the VXX since its inception have been the greatest short of all time? While the potential rewards can be lucrative, shorting VXX is a recipe for disaster. Any unexpected market event can trigger massive spike. Though the VXX has a negative correlation against SPY, its velocity is far greater. This could cause a significant dent in a trader’s portfolio with a short position. Remember the 2020 market crash? While the SPY fell 36% in 2020, high to low, VXX spiked more than 600%!

VXX’s price movements can be aggressive, with upside moves leading to potentially dramatic margin expansion. At the same time, with increasing risk to the upside, the brokerage firm might increase the margin requirement percent of short VXX positions, adding more pressure to the remaining fund to trade. Predicting short-term volatility movements is challenging, and such positions expose you to unlimited losses if volatility unexpectedly surges. Unlike long positions, where losses are capped at the initial investment, short positions have theoretically unlimited risk. Don’t even think about shorting volatility funds directly!

A Better Way to Short Volatility

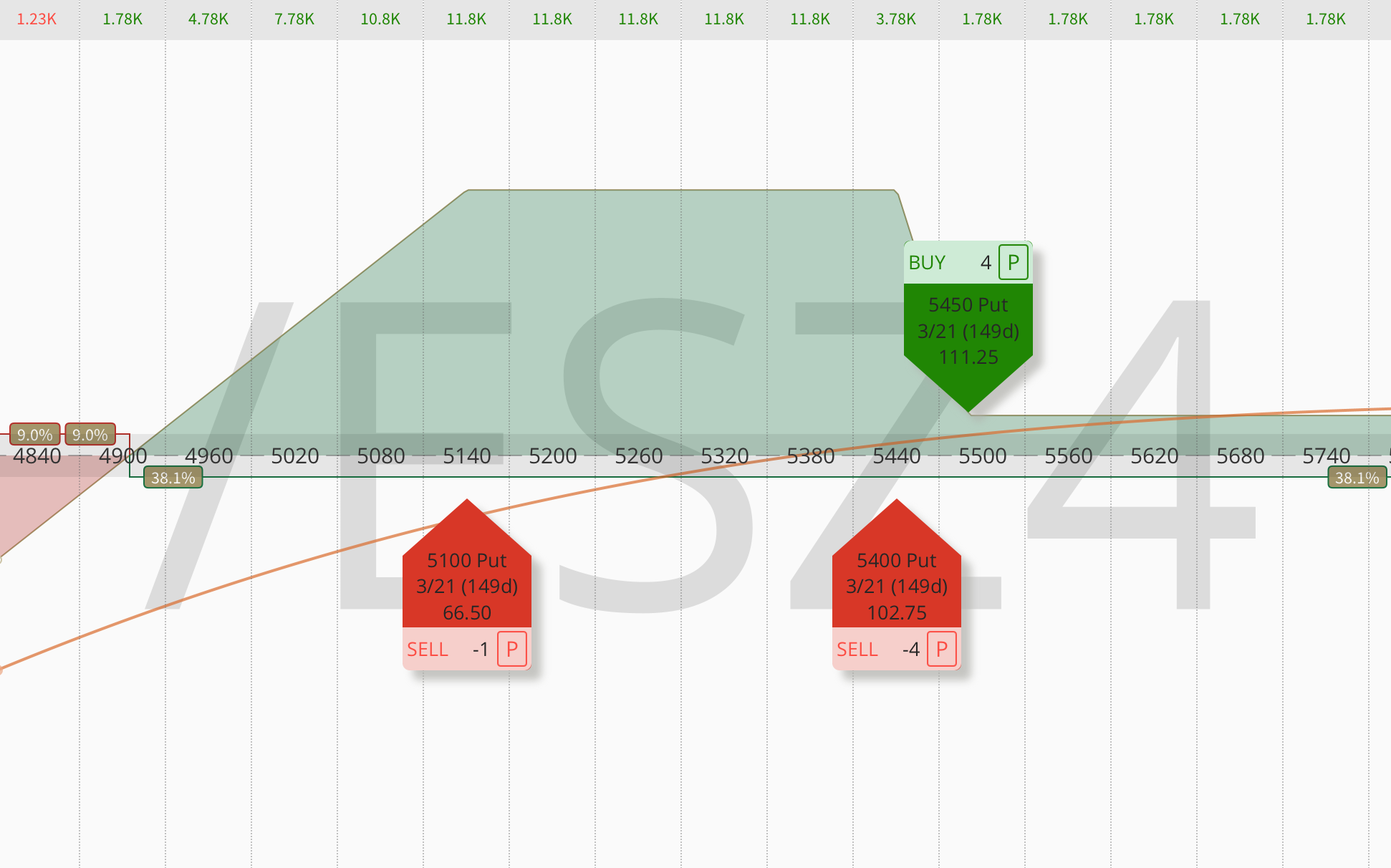

Instead of directly shorting VXX, consider alternative strategies that offer better risk-adjusted returns. A simpler approach is buying the SVIX, a one-times inverse volatility product held as a long position. This provides similar exposure to a decline in volatility without the drawbacks of shorting VXX directly. You can also use VXX options to profit from a potential VIX fall while limiting your risk. A basic strategy is buying put options on VXX, which gain value if VXX’s price falls as you anticipate. For advanced traders, there are more sophisticated options strategies like selling butterfly spreads using put options at three different strike prices to create a profit zone around an expected VXX price level.

In conclusion, volatility trading strategies can be a valuable addition to an advanced investor’s portfolio. However, it is still very important to understand the relationship of each volatility product so you have the knowledge you need to create a strategy that is best suited for you. VXX and similar products are designed for short-term hedging, not long-term holds. While VXX’s inherent price decay, without the reverse splits, could theoretically lead it to reach zero, the risk associated with shorting it directly far outweighs any potential reward. Instead, explore safer options trading strategies to find the approach that best aligns with your goals.