In investing, most strategies assume the market behaves in a “normal” way. Volatility stays within historical ranges, correlations hold, diversification works. Most of the time, those assumptions are good enough.

But anyone who has traded through 2008, March 2020, or the VIX spike of August 2024 knows that markets periodically stop behaving normally. In those moments, the rules break down simultaneously; correlations spike toward 1.0, diversification disappears, and positions that looked balanced in normal conditions turn into concentrated directional bets against you, all at once, without warning.

These are the events Nassim Nicholas Taleb called “black swans”. Rare, extreme, and devastating to unprotected portfolios. That’s why I run the Black Swan Hedge. It’s an options strategy designed to protect your portfolio from these unexpected tail risks. In this post, I’ll explain how the Black Swan Hedge works and why it’s essential for managing risk. I’ll also share some practical steps to help you implement it.

What Is a Black Swan Event?

Before diving into the hedge, it’s worth understanding the term precisely. A Black Swan event is a rare, unexpected occurrence with severe consequences. Popularized by Nassim Nicholas Taleb, the concept describes events that are nearly impossible to predict but carry an enormous impact when they occur. Think about the 2008 global financial crisis, the 9/11 attacks, the COVID-19 pandemic. These are all examples of Black Swan events.

Characteristics of Black Swan events:

- Rare: Highly improbable but not impossible.

- Impactful: Causes widespread financial, economic, or social disruption.

- Retrospectively predictable: After it happens, people claim they “saw it coming”.

For options traders, these events present a specific and serious challenge. During a Black Swan event, markets take a sharp dive and assets that typically move independently crash in unison. This correlation spike leaves even carefully diversified portfolios exposed to losses far beyond what the risk models predicted.

Why Do You Need a Black Swan Hedge?

Most traders design their portfolios with diversification in mind, spreading risk across asset classes and sectors. In a normal market, this strategy works because different assets often don’t move in sync – sometimes they even move inversely. But in extreme downturns, that safety net can vanish quickly.

When panic hits, investors sell off everything just to hold cash, and suddenly correlations between assets spike. The portfolio that looked genuinely diversified across five sectors becomes effectively a single large long-market bet. This phenomenon, known as a correlation spike, is what makes diversification strategies fail precisely when you need them most.

The table below, based on tastylive’s research, shows how correlations between common holdings and the S&P 500 (SPY) change as volatility rises.

| VIX Level | LUV | EEM | AAPL | XLE | COST | Avg. |

| Above 20% | 0.55 | 0.74 | 0.78 | 0.59 | 0.62 | 0.66 |

| Above 30% | 0.63 | 0.80 | 0.86 | 0.65 | 0.70 | 0.73 |

| Above 40% | 0.74 | 0.89 | 0.93 | 0.86 | 0.78 | 0.84 |

Here’s what the data shows:

- When the VIX exceeds 20%, the average correlation between these assets and SPY is 0.66, which is already elevated compared to normal market conditions.

- At VIX levels above 30%, correlations increase further, averaging 0.73.

- In extreme conditions, when the VIX exceeds 40%, correlations spike to an average of 0.84, with some assets like AAPL and XLE showing correlations as high as 0.93 and 0.86.

In plain English: during a severe market crash, almost everything you own starts moving together. Emerging markets, energy, consumer staples, technology – they all fall in concert. Relying solely on diversification to protect against extreme events is like assuming your house fire won’t spread to the next room.

What Is a Black Swan Hedge?

When diversification fails, a Black Swan Hedge steps in. Rather than managing day-to-day risk, this strategy uses options to guard specifically against those rare, catastrophic events. The key features of a Black Swan Hedge include:

- Downside protection: Profits when the market falls sharply.

- Low cost: Implemented with out-of-the-money options that are relatively inexpensive in calm markets.

- Crisis focused: Specifically designed to counteract extreme market events rather than everyday volatility.

The goal is a hedge that costs very little to carry in normal markets, and pays off massively when the rare event occurs.

Not Every Selloff Is a Black Swan

A 7% correction, a slow 20% bear market, and a volatility explosion are not the same problem. They require different hedges.

A slow bear market hurts portfolios through persistent directional drag. Positions bleed steadily, theta income slows, and the account grinds lower over weeks or months. A Black Swan hurts through speed, convexity, margin expansion, correlation collapse, and volatility explosion simultaneously.

That’s why a well-constructed portfolio usually needs layers. A correction hedge addresses slow declines. A Black Swan Hedge is specifically designed for the violent left-tail event. Confusing the two is why many traders buy disaster protection, watch the market grind 15% lower over six months, and wonder why the hedge didn’t pay – it was never designed to.

The Simplest Black Swan Hedge: Why It Fails

Remember The Big Short? The movie showed how Michael Burry made a bold bet on the housing market collapse by buying credit default swaps – financial instruments that acted like out-of-the-money puts – designed to soar in value when disaster struck.

This idea forms the basis of the simplest Black Swan Hedge: buying far OTM put options (often called teenies) on a major index like the S&P 500 to protect against a catastrophic crash. Traders typically buy these teenies for around $2 in premium or less, with expirations ranging from 30 to 90 days.

Here’s how it works:

- You purchase put options with strike prices well below the current market level, often 20% or lower.

- These options are cheap because the market believes a massive crash is highly unlikely.

- If a crash occurs, the value of these puts soars, helping offset losses in your portfolio.

In options lingo, the phrase “buy teenies to own Lamborghinis” captures the potential for huge windfall gains from these small, inexpensive options. While the concept is straightforward and the dramatic success stories like Michael Burry’s make it seem irresistible, this approach has several critical flaws for most traders:

- High long-term cost: Far OTM puts may seem cheap on their own, but the costs add up significantly over time. Since Black Swan events are extremely rare, most of these options expire worthless. And because long puts lose value over time due to negative theta, their cost erodes slowly but steadily, dragging down overall returns month after month.

- Extremely low probability of profit: Black Swan events don’t happen often. You’re paying for insurance against an event that might not occur for years, or even decades, making this strategy more like an expensive safety net than a practical investment.

- Inefficient coverage: This hedge only works in extreme scenarios. It offers little to no protection during moderate declines that can still significantly impact your portfolio. In 2022, the S&P 500 fell nearly 27% over a prolonged period rather than in a sharp crash. Far OTM puts expired worthless every month while portfolios declined steadily. The VIX reached elevated levels but never triggered the explosive spike that makes far OTM puts valuable.

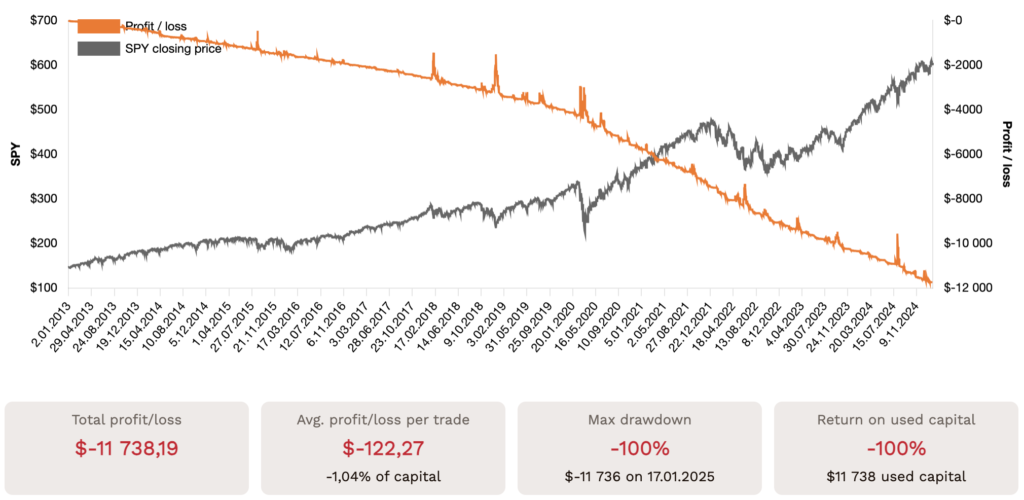

The backtested P&L of buying 10-delta SPY put options at 45 DTE illustrates this problem clearly; a slow, steady bleed in normal conditions with the payoff concentrated in rare events that may not arrive for years.

While this strategy worked remarkably well for Michael Burry during the 2008 crisis, it isn’t practical for most traders. The long-term costs, limited coverage, and inefficiency in handling typical market corrections make it more of a theoretical exercise than a sustainable hedge.

A Smarter Approach to the Black Swan Hedge

If you’ve found that simply buying OTM puts is slowly draining your portfolio, you’re not alone. I knew I had to find a better solution, so I asked myself: how could I protect against those rare, extreme events without bleeding cash over time? The hedge needed to be truly theta positive, one that gained strength as time passed. Ideally, it would scale to match the size of my standard at-the-money trades. And most importantly, I wanted it to be as cost-effective as possible, or essentially free.

That’s when I turned to the Black Swan Hedge. This strategy goes beyond just buying far OTM puts, and I’ve learned a great deal from traders like Ron Bertino, whose method uses a dynamic options setup that protects against major market moves while cutting down on the negative effects of time decay.

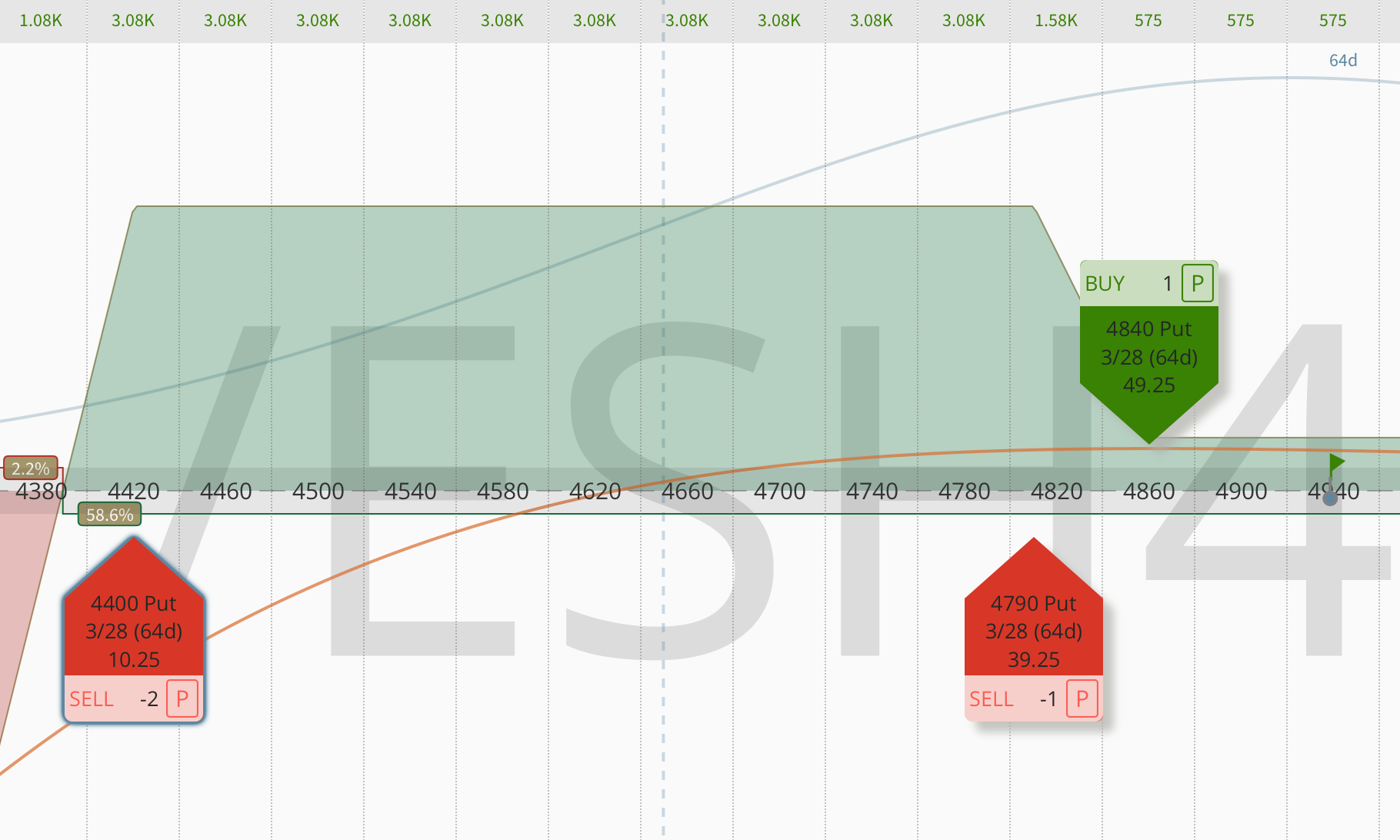

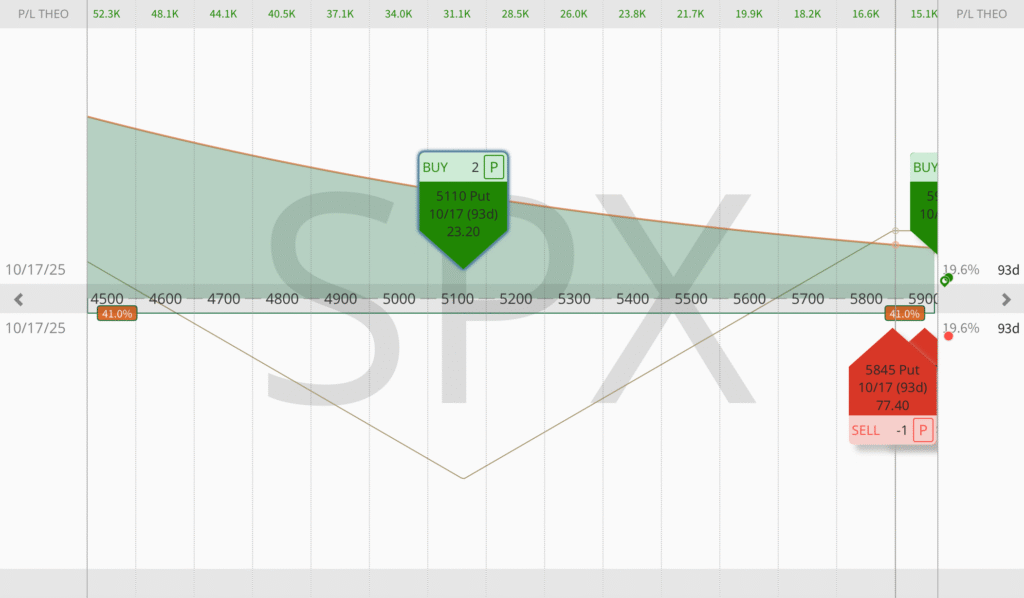

Here’s one example setup that works well, and there are many variations:

- Strikes: Sell three short /ES puts at around $3, and buy five long puts 50 points below the short strike to create a 3-to-5 backratio spread.

- DTE: Start by purchasing the Black Swan Hedge at about 120 DTE, ideally on a day when the market is up and volatility is calm.

- Short put harvest: Close the short puts when they reach $0.20 or at 14 DTE, whichever comes first. Then reopen the next tranche.

Remember: the Black Swan Hedge is primarily a vega and vanna hedge, with vanna being the rate of change of vega with respect to the underlying price. Running it as a campaign helps you manage tail risk systematically over time while keeping the cost of protection as low as possible.

There are many ways to implement this strategy, along with smart financing techniques that can keep the cost low, or even zero. I’ve developed a more sophisticated version of the Black Swan Hedge that actually lets you enter for a credit. With this setup, you can collect up to $10,000 if the market only sees a shallow correction, and potentially much more if a full-blown market Armageddon hits. The full details of the OptionsJive Black Swan Hedge structure are covered in my Trading Plan.

Black Swan Hedge vs. Teenies

In a backtest of the August 24, 2015 crash, where SPX dropped 236 points (11.24%) in five days and VIX increased 40 points (309%) in the same period, Ron Bertino compared a standard teenie position to a properly constructed BSH, entering both at nearly identical cost.

The teenies, purchased for $275, grew to $4,785 on August 24 – a fantastic return. The BSH, purchased for $280 (essentially the same cost), grew to $8,410. Nearly double the protection for the same initial outlay.

This isn’t just a matter of buying different puts. The BSH achieved this advantage primarily through higher positive vega; 149 for the BSH versus 94 for the teenies. In a crash, the volatility surge that accompanies the market decline amplifies the BSH’s gains far more than simple put buying. More positive vega means more benefit from every point the VIX moves upward.

The OptionsJive version improves on Bertino’s structure further. By entering for a net credit, the hedge costs nothing to carry in normal conditions. In calm markets, it runs for free, in a shallow correction, it generates income, and in a full crash, it pays off substantially. That’s the design goal: zero cost in normal markets, meaningful protection when it matters.

VIX Calls as a Portfolio Hedge

Beyond the BSH structure, there’s a second approach to black swan hedging worth understanding: buying VIX call options.

The CBOE Volatility Index measures the market’s expected 30-day volatility based on S&P 500 options pricing. It’s often called the “fear gauge”. It moves inversely to the S&P 500: when stocks fall sharply, VIX typically spikes. During the 2008 financial crisis, VIX surged above 80. During the March 2020 COVID crash, it exceeded 65 intraday. These are the conditions where VIX call options produce extraordinary returns.

Research shows that adding a small allocation (1% to 3% of portfolio value) to VIX calls can provide meaningful protection during market crashes. In months when no crash occurs, the calls expire worthless and you lose the small premium paid. In months when a crash does occur, the returns can be extraordinary. A single month’s profitable hedge can cover years of premium cost.

You can adjust the number of VIX calls you buy by looking at your portfolio’s overall risk, measured by its beta-weighted delta and short vega exposure, and by comparing them to SPY puts using a conversion ratio. Because VIX options have a $100 multiplier and respond to volatility rather than price direction, the sizing calculation requires accounting for the expected relationship between a market decline and the VIX spike that accompanies it.

One important nuance: VIX options are priced from VIX futures, not the spot VIX. The VIX futures market is typically in contango; futures trade above spot because the market prices in mean reversion to long-run volatility levels. This means theta decay on long VIX calls is more aggressive than many traders expect. During acute crashes, the term structure typically inverts into backwardation, which supports long VIX call values and amplifies the hedge payoff. Understanding this is critical for choosing the right strikes and expirations.

While VIX calls might not completely protect you from every type of downturn – they are most effective in sudden, sharp crashes rather than slow grinding bear markets – they offer a cost-effective and smart way to guard against those rare, extreme market moves that can otherwise be devastating to a short premium portfolio.

Summary

Black Swan events are very rare, but when they strike, they can wipe out an unprotected options portfolio in days. Just like car or home insurance, hedging may feel like a sunk cost most of the time. But when disaster hits, you’re glad it’s there.

Some traders argue that you should only risk a small portion of your net worth in the market. But most people’s capital needs to work, not sit idle. That’s exactly why the Black Swan Hedge matters. It allows you to deploy capital aggressively in normal conditions, collect premium systematically, and sleep at night knowing the catastrophic scenario is covered.

Teenies are one option. But if you want twice the payout for the same cost, and the ability to enter for a net credit, the Black Swan Hedge is the better choice.

As Tom Sosnoff says: the best hedge is staying small and using your buying power wisely. My Trading Plan outlines how to do both while preparing for the unexpected, including the full construction of the OptionsJive Black Swan Hedge, and how it integrates with the short premium strategies that generate the income. With this setup, you can collect up to $10,000 in a shallow correction, and even more in a full-blown crash.