Most traders who want to profit from a big, unpredictable market move reach for a long straddle. Buy an ATM call and an ATM put, wait for the underlying to move, collect. The logic is clean. The execution is simple. But there is one persistent problem.

You are paying full extrinsic value on both options. Every day the market stays calm, theta bleeds the position. In slow, grinding markets, the ones that precede many major moves, a long straddle can be half-dead by the time the catalyst arrives. You can be completely right about the direction and magnitude of a coming move and still lose money because the market took too long to get there.

The ZEEHBS was designed to solve this. Popularized by Tony Rihan, a tastytrade-affiliated options trader, the Zero Extrinsic Hedged Back Spread carries close to zero net extrinsic value at entry. Time is no longer working against you from the moment you enter. The theta bleed that kills most long volatility positions in slow environments is reduced to a fraction of its normal cost.

But the ZEEHBS is not a true straddle replacement, and calling it one is one of the most common misconceptions about the strategy. It is a long-biased, low-theta, convex structure that can profit from upside continuation or a large downside crash, while remaining vulnerable to moderate declines. That asymmetry, the thing that makes it different from a straddle, deserves precise understanding before capital goes to work.

What Is the ZEEHBS Options Strategy?

The Zero Extrinsic Hedged Back Spread is designed to generate alpha while providing a hedge against significant downside risk. Essentially, it’s a bullish strategy with built-in protection. It starts with the ZEBRA strategy – buying two in-the-money call options and selling one at-the-money call option – and adds a 50% delta hedge through a synthetic short position.

The ZEBRA itself achieves near-zero extrinsic value, meaning there is almost no time decay. It acts as a stock replacement, with price movement closely mirroring the underlying. To complete the ZEEHBS, you add a synthetic short by selling one ATM call and buying one ATM put at the same strike and expiration. This partial hedge limits downside risk and provides protection during significant price swings.

The result functions similarly to a long straddle; it profits from large moves in either direction, but with one critical structural difference: near-zero extrinsic value and dramatically reduced time decay. That is the edge. A standard long straddle bleeds premium daily, the ZEEHBS is designed to carry far less theta decay.

The strategy is usually implemented with a short time horizon. My personal preference is to execute this trade on Mondays, using options with 7 DTE. This approach takes advantage of the strategy’s quick, big moves in either direction. It can generate strong profits when these moves happen, but it also limits losses when they don’t.

Why Use ZEEHBS?

Low extrinsic value. Unlike a traditional long straddle, ZEEHBS eliminates most of the extrinsic value, dramatically reducing the risk associated with options time decay. The majority of the premium paid is intrinsic; real, immediate value that does not decay. This makes the strategy viable in slow markets where a straddle would bleed to death.

Tail risk hedging. The synthetic short’s long put provides protection against extreme negative price moves, protecting the portfolio in sharp downturns while allowing gains if the market bounces back. It is not unlimited protection, the valley of death discussed below is a real risk, but it transforms a pure long-biased position into one that can survive and profit from a crash.

Alpha generation in volatile conditions. Unlike static hedges or long-only positions, ZEEHBS benefits from price extremes, particularly during earnings releases, economic announcements, or any event expected to induce significant market swings. The research supports this. More on the numbers shortly.

The Real Edge: Path, Not Prediction

Before looking at the mechanics, there is a more important conceptual point to internalize.

The ZEEHBS is not simply a bet that SPY will move. It is a bet on how SPY moves. A steady grind higher works well; the position carries positive delta, so upside drift generates consistent gains. A violent crash works if it is large enough to push the long put deep in-the-money. What hurts is a slow, moderate, persistent decline; one where the long calls lose value gradually without the crash magnitude needed for the put to compensate.

This also clarifies why entry timing matters more than directional conviction. When you enter a ZEEHBS, you are not predicting where SPY will be in five days. You are selecting conditions where the right paths – up meaningfully, or down dramatically – are more probable than the wrong one: moderate, slow, sustained decline.

What You Are Actually Exchanging

A long straddle loses money through visible, predictable theta decay. You watch it bleed every day the market sits still. The ZEEHBS reduces that theta bleed dramatically, but the cost shows up elsewhere, in the valley of death. You are not getting a free straddle. You are exchanging constant time decay for a specific payoff hole in moderate declines. The risk has been transformed, not removed. Understanding this reframing is what separates traders who deploy the ZEEHBS intelligently from those who get caught off guard.

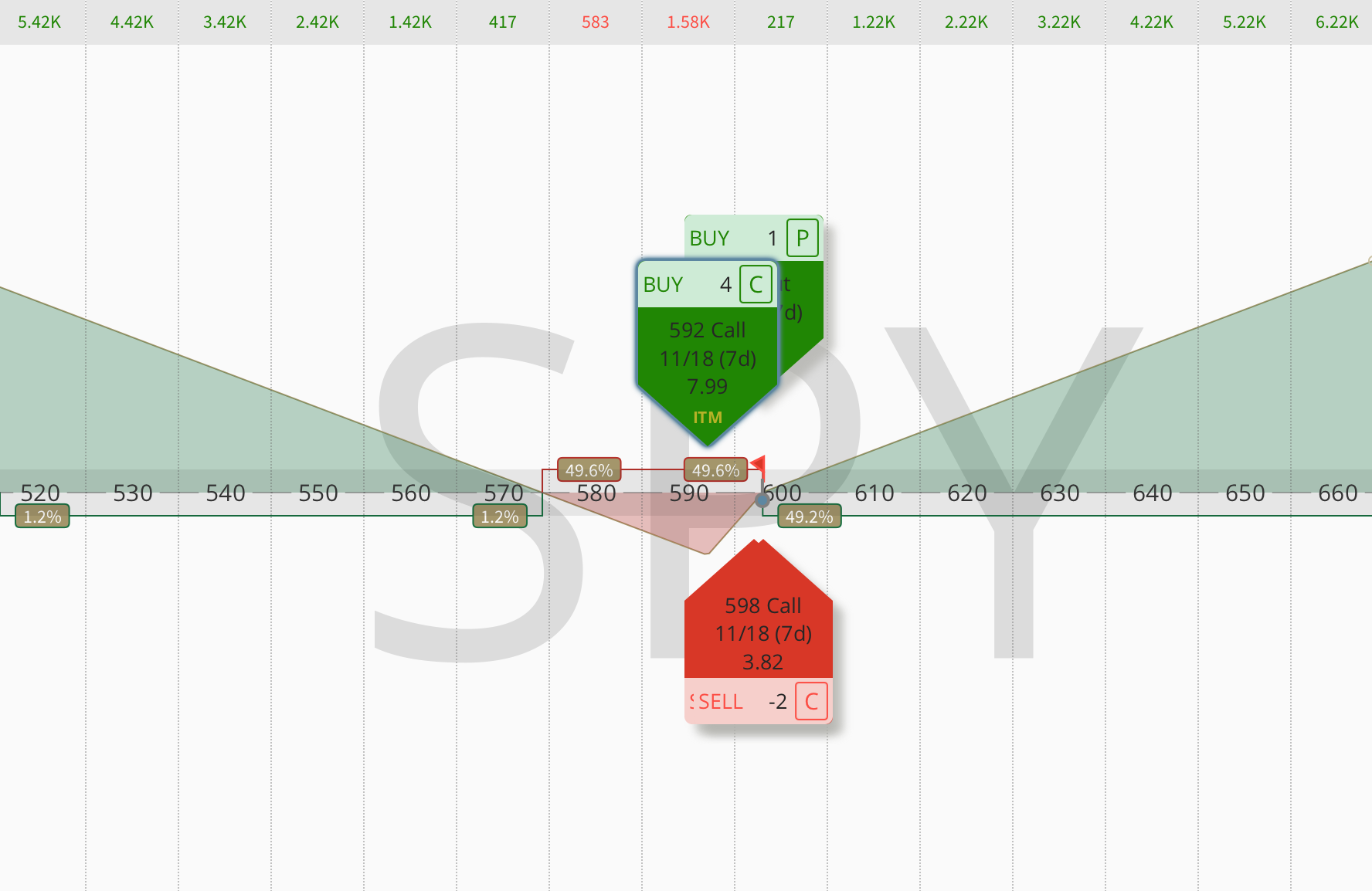

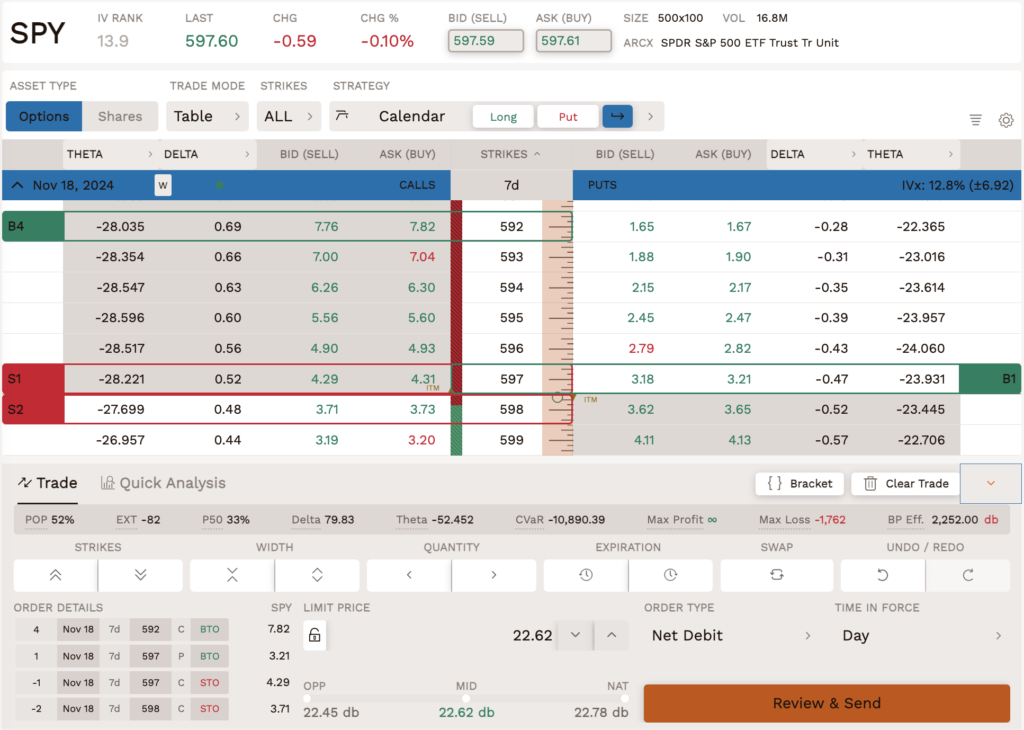

The Full Construction: A Live SPY Example

The ZEEHBS has three components built in sequence. Here is exactly how they fit together, using a real trade with SPY at $597.60 and 7 days to expiration.

Step 1: Build two ZEBRAs.

The ZEBRA buys two ITM calls and sells one ATM call, with strikes chosen so that two times the extrinsic of the long calls approximately equals the extrinsic of the short ATM call. With the $598 ATM call carrying $3.72 of extrinsic, each long call needs approximately $1.86 of extrinsic. The $592 strike fits; it carries $2.19 of extrinsic at a cost of $7.79, with a delta of approximately 0.70. Two ZEBRAs means: buy 4 × $592 calls, sell 2 × $598 calls.

Step 2: Add the synthetic short.

Sell one additional ATM call and buy one ATM put at the $597 strike. This hedges approximately 50% of the position’s delta. The total position is now: 4 long $592 calls, 3 short $598 calls, 1 long $597 put.

Step 3: Verify the extrinsic offset and model the payoff.

Total debit: approximately $2,300 per spread.

Place all legs as a single multi-leg order. Never leg in separately; the extrinsic offset depends on simultaneous fills.

Understanding the Debit and Maximum Loss

The total debit paid is approximately equal to the intrinsic value of the four long calls, because the net extrinsic portion of the trade cancels to near zero.

The debit is not the maximum loss. This is a common error that needs to be stated clearly. The ZEEHBS is a defined-risk position, but the true worst-case loss needs to be read from the position’s modeled payoff diagram, not assumed to equal the debit paid. The long put retains value throughout the range of outcomes and can reduce the realized loss compared to the raw debit figure. The worst-case loss occurs in the valley of death zone, where long calls have lost most of their value but the long put has not yet generated significant intrinsic value.

Always model the position in your broker’s risk analysis tool before entering. The payoff diagram tells you the actual maximum loss, the valley depth, and the breakeven thresholds on both sides. Trading the ZEEHBS without this visualization is operating with incomplete information.

The Valley of Death: The Primary Risk

The valley of death is the price range where the strategy experiences its maximum loss. It occurs when the underlying declines moderately, falling below the long call strikes but not far enough to generate meaningful gains from the long put.

Specifically: the four long ITM calls lose value as they drift toward or below ATM. The long put gains some intrinsic value, but not enough to offset the call losses. The short calls lose value, which is favorable, but this benefit is smaller in magnitude than the call losses. The net effect is a position that can show losses disproportionate to the magnitude of the move.

This is not a modeling error; it is the inherent structural consequence of the zero-extrinsic design. You paid primarily for intrinsic value on the upside. In moderate declines, that intrinsic value deteriorates before the crash hedge activates meaningfully.

My battle-tested adjustments when the valley approaches

Re-center the ZEBRA. Close the existing long calls and reopen them at lower strikes centered around where SPY is now trading. This resets the position to a new structure appropriate for current prices and moves the valley down with the underlying. Act before maximum loss is approached, not after.

Sell an OTM call. Adding a short call above the current price collects additional credit and reduces the net cost basis. It caps some upside potential but provides immediate relief. Most appropriate when you believe the decline may continue at a moderate pace.

Roll the long calls down. Shifting the long ITM calls to lower strikes without closing the entire structure adjusts the position’s sensitivity downward while preserving the put hedge.

Sell the long put. Removing the put converts the trade toward a more directional bullish structure. Downside loss remains limited by the remaining cost basis, but you lose the feature that allowed the position to recover in a genuine crash. Use this only when you believe the decline is temporary and a sharp rally is imminent.

Close the position. Sometimes the right adjustment is no adjustment. If the market is trending persistently against the position, taking the defined loss and moving on is better than layering adjustments that add cost without changing the fundamental situation.

My Trading Plan includes additional battle-tested adjustments calibrated to specific scenarios, particularly the difference between managing a position that enters the valley during a sharp one-day drop versus a slow multi-day grind.

Assignment Risk in SPY

Because the ZEEHBS is often built in SPY, traders must account for a risk that does not exist in European-style index options: early assignment on the short calls.

SPY options are American-style. Short options can be assigned before expiration at any point, not just at expiration. The three short ATM calls in the ZEEHBS are particularly vulnerable in two scenarios.

Low extrinsic value. As the trade ages and short calls move into the money with little time remaining, extrinsic value shrinks toward zero. When a short call carries $0.05 of extrinsic and $2.00 of intrinsic, the economic incentive for the call holder to exercise early and capture that intrinsic value immediately increases substantially.

Ex-dividend dates. Call holders exercise short-term ITM calls to capture SPY’s quarterly dividend. If the dividend exceeds the remaining extrinsic value in the short call, early exercise is rational. Always check the ex-dividend calendar before entering any position with short calls in SPY.

Early assignment on one leg changes the position operationally. Instead of three short calls, you may find yourself short 100 shares of SPY with two short calls still open. The remaining legs still provide coverage, but the position requires immediate attention and may create unexpected margin impact.

Traders who want to eliminate this risk entirely can use European-style index options such as SPX. SPX options cannot be assigned before expiration by definition. The trade-off is a higher notional value per contract (SPX is approximately 10x SPY) and cash settlement at expiration rather than share delivery.

Performance: The Research

Research conducted by Gage Marsan and James Xu, published as part of the Quant@Illinois SP24 Trading Project, provides a comprehensive backtest of the ZEEHBS strategy from January 2021 to January 2024. The period includes the low-volatility bull market of 2021, the sustained bear market of 2022, and the recovery of 2023; a meaningful range of conditions. Here are some key metrics.

| Strategy | Return | Max Drawdown | Win Rate | Sharpe Ratio |

| SPY (buy-and-hold) | 35.06% | -23.93% | n/a | 0.5 |

| Modified ZEEHBS | 42.61% | -9.8% | 77% | 0.554 |

Implementing ZEEHBS: Key Principles

Choose the right underlying. Assets likely to experience volatility spikes – major indices, large-cap tech, or anything with upcoming binary events – are prime candidates. Liquidity is essential. On a 7-leg position, wide bid-ask spreads on even one leg can meaningfully erode the zero-extrinsic property and inflate the real cost of entry.

Market timing matters. Deploy the ZEEHBS when the market is calm but a catalyst is approaching. FOMC days, CPI releases, earnings weeks for major index components – these are the environments where the path dependency works in your favor. A market that is already moving aggressively in one direction is less suited for entry than one that is compressed and building tension.

Low implied volatility is the ideal entry condition. When IVR is below 15, the long puts and calls are cheaper, the debit is smaller, and the risk-reward improves. Entering when IV is elevated means paying elevated premiums that may crush against you before any move materializes; combining the straddle’s theta problem with the ZEEHBS’s valley risk.

Review the position regularly. If the underlying moves sharply upward, recalibrating the hedge can optimize returns. If it drifts into the valley, adjustment is necessary.

Is ZEEHBS Options Strategy Right for You?

The ZEEHBS is not a beginner’s strategy. It requires a solid understanding of options mechanics, active management discipline, and the ability to execute a 7-leg position under real market conditions. However, for experienced traders, it offers a unique balance of alpha potential and downside protection that very few strategies can match.

The research backs it. The 77% win rate over three years, the -9.80% maximum drawdown versus -23.93% for SPY, the Sharpe ratio advantage; these are not marketing claims. They are the output of independent academic research on live market data covering multiple market regimes.

If you’re looking to enhance your portfolio’s performance in volatile markets, ZEEHBS is worth exploring seriously. In today’s unpredictable environment, strategies that generate alpha while managing tail risk are exactly what a sophisticated options portfolio needs. With the right preparation, the right entry conditions, and battle-tested adjustments in place, this can be one of the most powerful tools in your options trading arsenal.

The OptionsJive Trading Plan covers the full ZEEHBS adjustment playbook; how to manage the valley across different market environments, when to re-center versus close, and how the position fits alongside the short premium strategies that generate the portfolio’s core income.

Frequently Asked Questions

What does ZEEHBS stand for?

Zero Extrinsic Hedged Back Spread. Each word describes a structural feature: Zero Extrinsic (net extrinsic value at entry is approximately zero), Hedged (the back ratio is hedged with a synthetic short), Back Spread (a back-ratio spread using calls).

Who created the ZEEHBS strategy?

Tony Rihan, a tastytrade-affiliated trader and options educator. The strategy was presented on the tastytrade network.

Is the ZEEHBS a straddle replacement?

No. It borrows the “profit from large moves” concept but is not symmetric. The ZEEHBS starts with positive delta (+50 to +100), is long-biased, and has a valley of death in moderate declines that a standard straddle does not. It is a long-biased, low-theta, convex structure, not a neutral volatility instrument.

How is it constructed?

Two ZEBRA spreads (4 ITM calls at 70 delta, 2 short ATM calls at 50 delta) combined with one synthetic short (sell 1 ATM call, buy 1 ATM put). Total: 4 long ITM calls, 3 short ATM calls, 1 long ATM put, executed at 7 DTE as a single order.

What is the maximum loss?

The ZEEHBS is defined-risk, but the true maximum loss must be read from the modeled payoff diagram, not assumed to equal the debit paid. The long put retains value across most scenarios and can reduce the realized worst-case loss. Always model the position before entering.

What is the valley of death?

The moderate decline zone where the position suffers its worst P&L. Long calls lose value as they drift below ATM, while the long put has not yet generated significant intrinsic value to offset. Large crashes and upside moves both benefit the strategy. Moderate declines do not.

Does the ZEEHBS have assignment risk?

Yes, when built in SPY. SPY options are American-style, meaning short calls can be assigned before expiration, especially when extrinsic value is low or around ex-dividend dates. Traders who want to eliminate this risk can use European-style SPX options instead.

What does the backtest show?

The Quant@Illinois backtest (Marsan & Xu, 2024), January 2021 to January 2024: Modified ZEEHBS returned 42.61% with -9.80% max drawdown and 77% win rate versus SPY’s 35.06% return and -23.93% max drawdown. Sharpe ratio 0.554 versus 0.50 for SPY.

When should I trade the ZEEHBS?

Low implied volatility environments (IVR below 15), 7 DTE, ahead of expected binary-outcome events where large movement is anticipated but direction is uncertain. My personal approach: enter every Monday, manage actively throughout the week.