“Buy the guts, sell the wings” is a key phrase for every short premium trader. If you’ve traded short strangles for some time, you know how a normal position can become uncomfortable. You sold a 16-delta strangle with plenty of room on both sides. The underlying moved, and your position started getting tested. Standard defense: you rolled the untested side toward the money. This helps you earn extra credit and lower your delta. That’s the main defense in the Trading Plan.

But if the underlying keeps going, you roll the untested side again. And again. At some point, the short call has moved so close to the short put that you’re looking at a straddle (both strikes ATM) or even an inverted strangle, where the call has crossed below the put and the strikes have swapped sides. You now have a short put above and a short call below. The position has drifted far from where it started.

This is not a failure of the strategy. It’s what active strangle management looks like in a trending market. But it creates a specific problem: your position is now highly concentrated around the current price, your gamma is elevated, and any significant move in either direction will hurt. The position needs to be restructured. This is the moment for “buy the guts, sell the wings.”

Where “Buy the Guts, Sell the Wings” Comes From

The phrase is widely associated with Tom Sosnoff of Tastylive, and it describes a specific position management adjustment, not an entry strategy. You don’t open a trade by buying the guts. You use this when an existing position has evolved, through defense and rolling, into a straddle or inverted strangle that needs to be repositioned.

The Mechanics: What You Actually Do

The adjustment is two simultaneous actions, paired with a roll out in time to a further expiration:

- Buy to close the ATM straddle or inverted strangle (the guts). These are the short strikes currently sitting at or near the money, compressed tightly around the current price. Whether you have a proper straddle (both strikes equal) or an inverted strangle (strikes crossed), you’re buying both legs to close. Yes, you’re paying full or near-full premium to exit them. That’s the price of the adjustment.

- Sell to open a new OTM strangle (the wings). Simultaneously, you sell a fresh short call above the current price and a fresh short put below it, both properly out of the money relative to where the underlying is right now. You do this in a further expiration (typically the next monthly cycle) to collect enough premium on the new strikes to cover the cost of buying back the guts and ideally bring in a small net credit on the overall roll.

- The result: you’ve closed the concentrated, high-gamma, near-the-money structure and opened a properly centered OTM strangle with room on both sides and a full new theta cycle working in your favor.

Why You Roll Out in Time

The further expiration is what makes the math work. ATM options carry maximum extrinsic value. Buying them back is expensive. OTM options in the current expiration may not carry enough premium to offset that cost. But OTM options in the next monthly cycle carry a full cycle of time value (theta). Selling the wings there gives you enough premium to close the straddle without paying a significant net debit, and ideally, to collect a small net credit that extends your breakeven on the overall trade.

If the numbers don’t work for at least a scratch, either go further out in time or reconsider whether this trade is worth continuing. Paying a meaningful net debit to restructure a losing position compounds the problem.

From Straddle to Fresh OTM Strangle

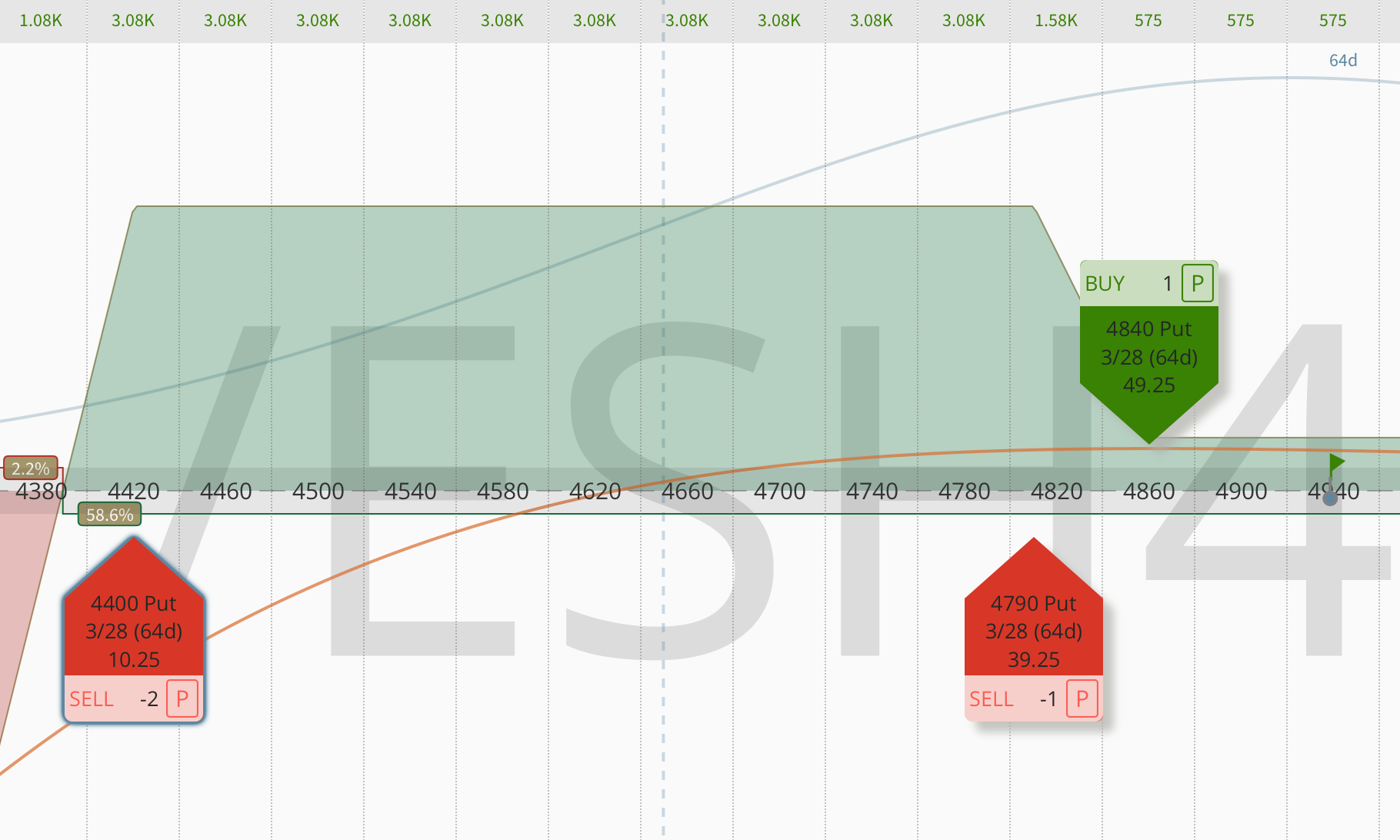

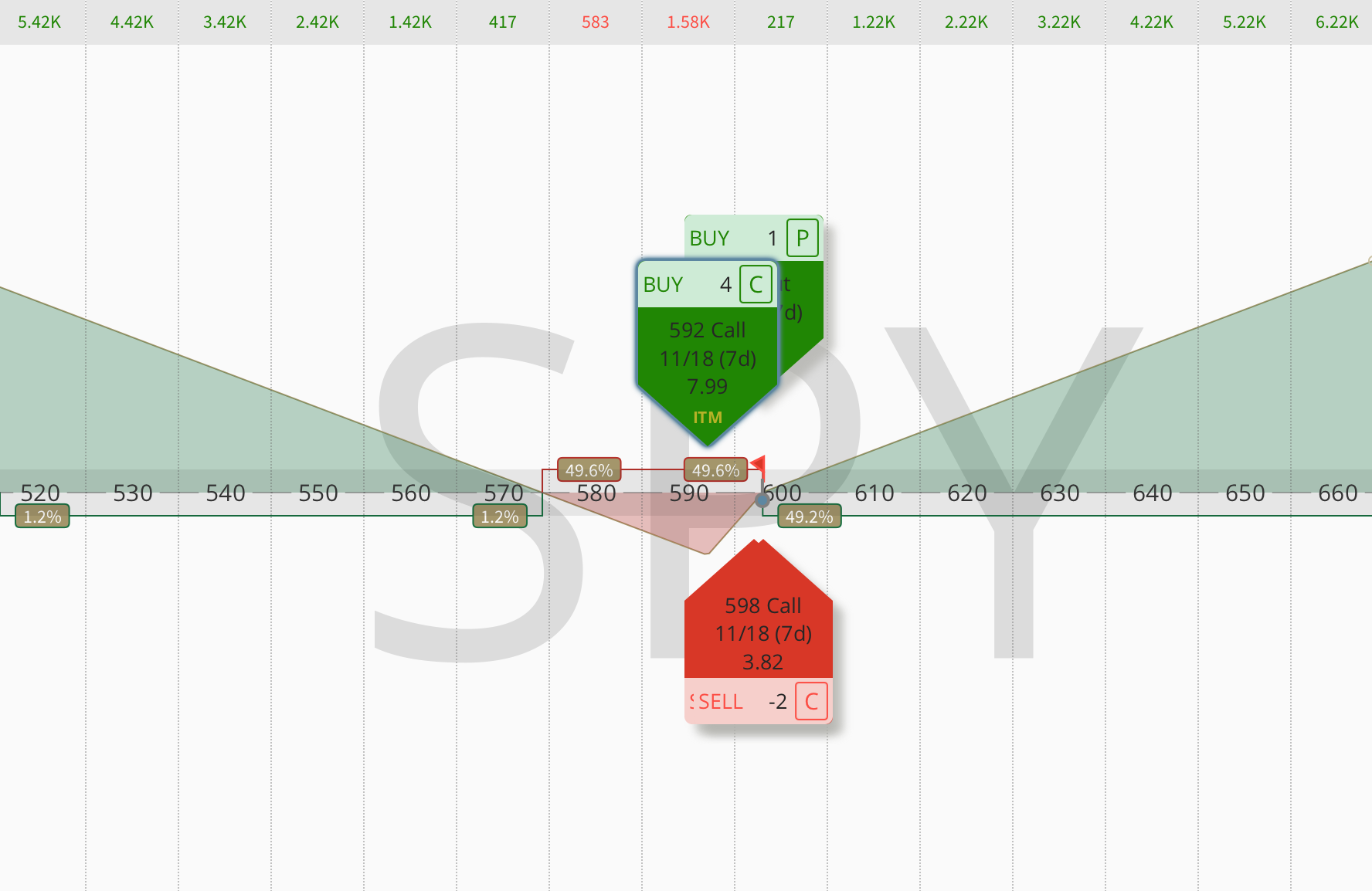

SPY is at $540. You sold a strangle: short the $520 put and short the $560 call. SPY dropped steadily, testing your short put. You defended correctly each time by rolling the untested call side down for credit: from $560 all the way down to $520 over several rolls, finally matching the put strike. Both legs are now short the $520 strike. SPY is at $518.

Your position:

- Short $520 put

- Short $520 call

- SPY at $518

That’s a straddle. Both strikes are identical, sitting just above where SPY is trading. Very high gamma. Any significant move in either direction hurts immediately. So, you decide to buy the guts and sell the wings.

You buy to close both legs, the $520 put and the $520 call, paying the current market price for each. Simultaneously, in the next monthly expiration, you sell a new $500 put and a new $545 call, centered around where SPY is now trading. The new OTM strangle premium collected covers the buyback and brings in a net credit of, say, $0.40.

You’ve gone from a straddle with no room to move to a properly positioned strangle with a full new expiration cycle and $20 of room on the put side and $27 on the call side. The trade is alive, restructured, and working again.

The Same Adjustment for an Inverted Strangle

When the strikes have actually crossed, your short call is below your short put; the adjustment works identically. You buy to close both legs of the inverted position and sell to open a new OTM strangle in the next expiration centered on the current price.

The inverted strangle has some useful properties: you’re collecting credit from both sides and your breakeven zone sits between the two crossed strikes, but it’s fragile. Any decisive move outside the narrow corridor between the crossed strikes hits you hard. Buying the guts and selling the wings is one of the cleanest ways out: instead of continuing to defend with more rolls that tighten the structure further, you close the whole compressed position and open a fresh one with proper room on both sides.

When rolling out of an inverted strangle, you may be paying a larger debit to close since both legs can carry near-intrinsic value. This makes the roll out in time even more critical; you need the further expiration to generate enough OTM premium to make the numbers work.

What to Watch For in Execution

Target a net credit or scratch. If the adjustment requires a significant net debit, either go further out in time or consider closing the position outright. There are situations where taking the loss cleanly is better than paying to roll into another structure.

Don’t tighten the new wings to force a credit. The temptation is to sell the new strangle close to the money to maximize the premium collected. Resist it. The entire purpose of this adjustment is to give yourself room. If you sell the wings too close, you’ll be back in the same compressed situation within days.

Track your total credits collected. Know the cumulative credit across the original trade and all subsequent rolls. That cumulative credit is the closest thing to your campaign cost basis and tells you how much room you’ve bought yourself. If total credits are still meaningful, the adjusted position has a real edge. If you’ve already given most of the premium back through rolling costs and this roll adds another debit, closing may be the right call.

This doesn’t fix a broken trade. If the underlying is genuinely trending hard in one direction, buying the guts and selling the wings gives you a wider OTM strangle, but the market will still be moving against you. The adjustment buys time and reduces gamma; it doesn’t reverse the underlying. If the fundamental premise of the trade is wrong, no roll saves it.

The Discipline Behind the Technique

What this technique represents is knowing when to stop defending the existing structure and when to step back and rebuild.

Rolling the untested side is the correct defense, right up until the point where the strikes have converged so tightly that the position no longer has room to work. Continuing to roll at that stage is stubbornness masquerading as management.

Buying the guts and selling the wings is the honest acknowledgment that the current structure isn’t working anymore. The position has evolved through legitimate defense into something that needs to be rebuilt from where the market is now, not where it was when you entered. You close the compressed inner position, open a fresh outer position, roll out in time, and let theta do its work again.

That’s active position management. That’s what buy the guts, sell the wings has described. The OptionsJive Trading Plan details the complete adjustment playbook. It explains when to roll the untested side, when a straddle conversion is smart, when to buy the guts and sell the wings, and when to close everything – download it here.