Most traders who want to get long on a stock face the same problem. Buying 100 shares is expensive, sometimes prohibitively so. Buying a call is cheaper, but comes with a fundamental drag: you pay extrinsic value at entry, and that value bleeds away every day whether the stock moves in your favor or not. Even if you’re right on direction, you can lose money if the stock doesn’t move fast enough.

The ZEBRA options strategy solves this directly. It gives you near-100 delta stock exposure, close to the same dollar-for-dollar participation in an upward or downward move as owning shares, at a fraction of the capital required, and without the extrinsic value drag that punishes most options buyers. The maximum loss is defined before you enter. The breakeven sits at or very near the current stock price, and the upside is unlimited, just like stock.

It is a stock replacement strategy that actually replaces stocks.

What ZEBRA Stands For

ZEBRA is an acronym: Zero Extrinsic Back Ratio (sometimes stated as Zero Extrinsic Value Back Ratio Spread). The name describes exactly what the structure achieves: a back ratio spread constructed so that the net extrinsic value of the position is approximately zero.

The strategy was coined by Liz Dierking and Jenny Andrews on their tastytrade show Calling All Millionaires, where they developed and popularized it as a practical stock replacement tool. It was also presented in detail in the first version of my Trading Plan.

The Core Construction

The ZEBRA has three legs, all using options of the same type: all calls for a bullish position, all puts for a bearish one, and the same expiration:

Buy two in-the-money options at approximately the 70-delta strike. Deep enough to have substantial intrinsic value, but not so deep that the bid-ask spread becomes prohibitive.

Sell one at-the-money option at approximately the 50-delta strike. Close to the current stock price, where extrinsic value is at its maximum.

The mathematics work as follows. Each of the two long ITM options carries some extrinsic value, typically around half of what the ATM option carries. By buying two of them and selling one ATM option, the extrinsic value you pay on the long side is offset by the extrinsic value you collect on the short side. The position nets to approximately zero extrinsic value (hence the name).

The result is a position whose breakeven sits at or very near the current stock price. If the stock is at $100 when you enter, the position starts profiting almost immediately on any upward move, rather than requiring the stock to overcome a premium hurdle as a naked call buyer must.

The Two Bullish Phases

Understanding the ZEBRA’s payoff profile requires understanding that it has two distinct phases of bullish behavior, and most explanations of this strategy stop short of making this clear.

Phase 1: Between the long strike and the short strike. In this zone, you hold two long calls and one short call. The net delta exceeds 100 because the two longs are gaining delta faster than the short is losing it. The position is effectively supercharged; it moves more than dollar-for-dollar with the underlying. This is the most dynamic and profitable phase of the trade, and it is why the ZEBRA can outperform stock ownership on a moderate upward move.

Phase 2: Above the short strike. Once the stock moves through the short ATM strike, the short call begins to offset one of the two long calls more aggressively. The net delta compresses back toward 100; the position behaves more like plain stock ownership again. Crucially, the upside here is not capped. I explicitly describe the ZEBRA as having “all of the upside profit potential” of stock. The position continues to profit above the short strike, just with a delta profile closer to 100 rather than the supercharged profile of Phase 1.

This two-phase structure is what makes the ZEBRA genuinely interesting. You get a supercharged delta kick on the initial move, an embedded stop loss if wrong, and unlimited upside if the stock keeps going.

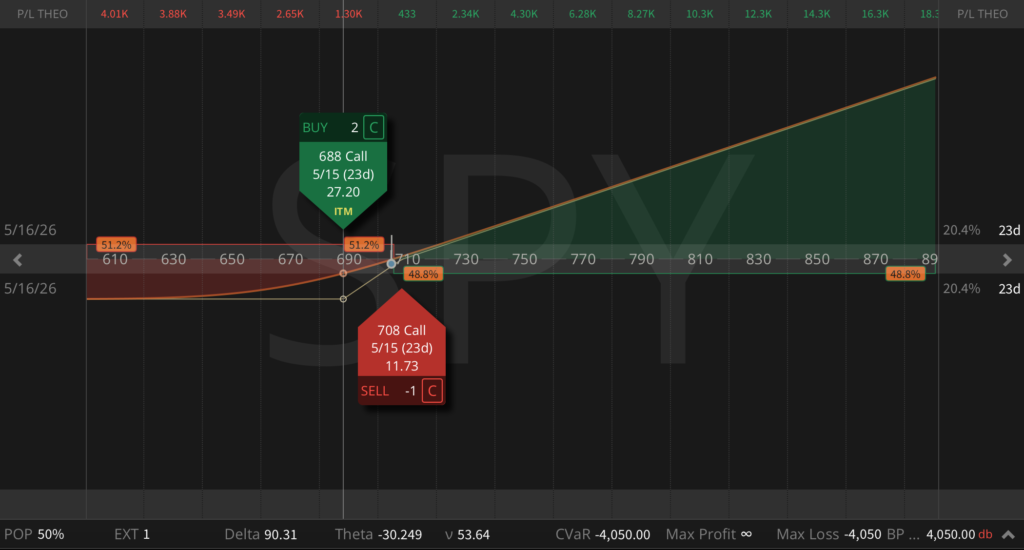

The Call ZEBRA: Bullish Version

The call ZEBRA is used when you have a strong bullish view on a stock or ETF.

Construction:

- Buy 2 ITM calls (~70 delta)

- Sell 1 ATM call (~50 delta)

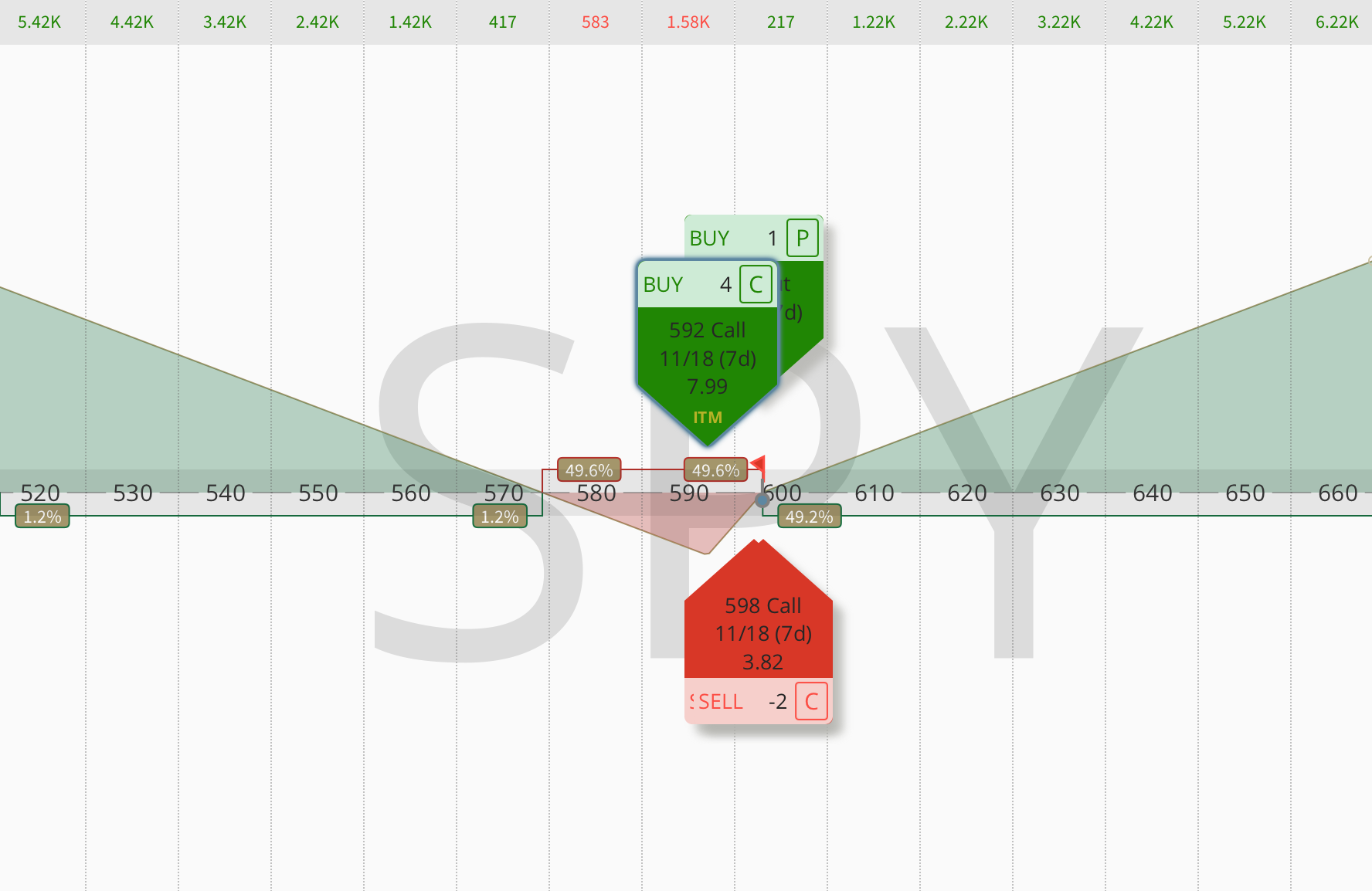

The net position carries approximately 90 to 100 long deltas, close to owning 100 shares, at a fraction of the cost. My SPY example above illustrates the capital efficiency: a call ZEBRA in SPY costs roughly $4,050 in buying power, providing approximately 90 deltas of exposure compared to buying 100 shares of SPY which requires $70,000 or more. Same directional participation. Roughly one-seventeenth of the capital.

The built-in stop loss comes from the structure itself. If the underlying moves against you, the position loses delta progressively; losses slow and eventually cap at the initial debit paid. The position behaves like a married put: defined maximum loss, unlimited upside.

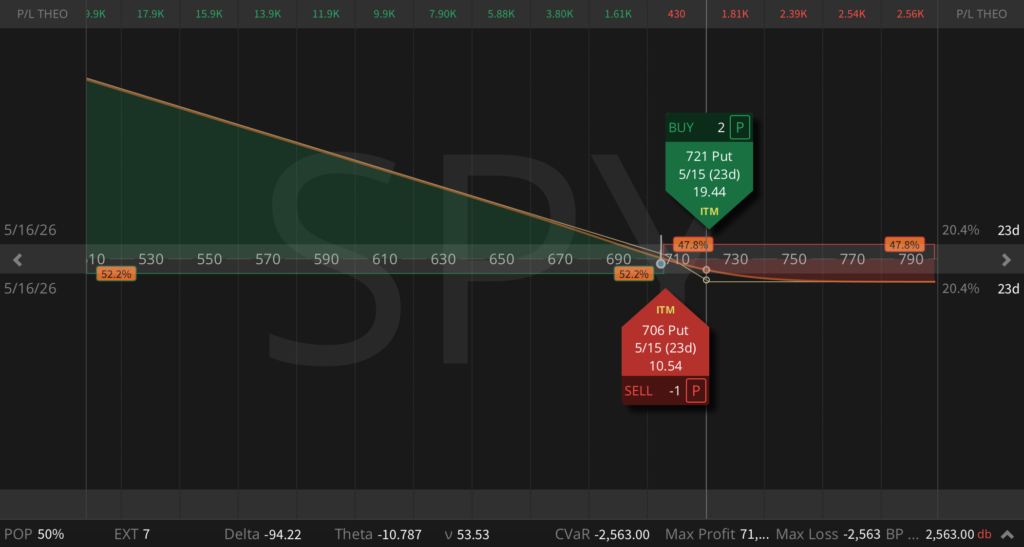

The Put ZEBRA: Bearish Version

The put ZEBRA is the mirror image – a bearish position that replicates short stock exposure with defined risk.

Construction:

- Buy 2 ITM puts (~70 delta)

- Sell 1 ATM put (~50 delta)

The net position carries approximately -90 to -100 deltas, behaving like short stock. The maximum loss above the upper long put strike is the debit paid. Below the ATM short put strike, the position profits nearly dollar-for-dollar with the decline in the underlying.

The capital efficiency on the short side is equally compelling. A put ZEBRA in SPY costs approximately $2,800 in buying power, compared to $15,000 required for shorting 100 shares of SPY outright using standard margin. For traders who want to express a bearish view without the capital requirements of short stock, the put ZEBRA is one of the most efficient structures available.

Why Zero Extrinsic Value Matters

Here is how the math works in practice, using a stock at $100:

| Leg | Strike | Delta | Action | Extrinsic Value |

|---|---|---|---|---|

| Long call | $94 | ~70 | Buy 2 | ~$2.00 each |

| Short call | $100 | ~50 | Sell 1 | ~$4.00 |

| Net extrinsic | ~$0 |

The $4.00 of extrinsic value paid on the two long calls is offset by the $4.00 collected on the short ATM call. The net cost of the position is almost entirely intrinsic value. This is what puts the ZEBRA’s breakeven at the current stock price, just like owning stock.

When you buy a single ATM call, you pay full extrinsic value and need the stock to move enough and fast enough to overcome that hurdle before you profit. When you buy a deep ITM call, you pay less extrinsic but get a lower delta. The ZEBRA solves both problems: near-100 delta from the two longs, extrinsic drag neutralized by the short.

The Role of Volatility and Skew in ZEBRA Setup

This is where the strategy becomes more nuanced than most introductions suggest, and where the entry quality can vary significantly depending on market conditions.

Low implied volatility is the ideal environment for both call and put ZEBRAs. The reason is in low IV environments options are cheaper. The ITM long options cost less, the ATM short option offsets enough, and the net debit is smaller. You can often go further out in time without dramatically increasing the cost of the position, giving your directional thesis more room to play out.

In high IV environments, the debit widens, and while the short ATM option collects more premium, the long ITM options also cost significantly more. The setup can still work, but it requires more capital and carries more risk if the trade goes wrong.

Skew affects how cleanly the extrinsic offsets. Put skew, the structural richness of OTM puts relative to calls in equity markets, affects the ZEBRA setup differently for calls versus puts. In a steep skew environment, the put ZEBRA may set up more cleanly than the call ZEBRA, because the ATM put collects more extrinsic value relative to the ITM long puts. Conversely, in a call skew environment, which appears in certain commodity underlyings or during meme stock periods, the call ZEBRA may set up more favorably.

Before entering a ZEBRA, verify that the extrinsic value relationship between your long and short options holds. Skew can shift this relationship enough that the position is no longer truly zero extrinsic; you may be paying a net extrinsic debit instead.

The Greeks of a ZEBRA Position

Understanding how the Greeks behave is essential for knowing when the position is working as designed and when it needs attention.

Delta: The ZEBRA starts with approximately 90 to 100 net deltas (call version). As discussed, delta exceeds 100 between the long and short strikes, then compresses back toward 100 above the short strike. If the stock moves against you, delta decreases progressively as the long options lose delta faster than the short; the position becomes less sensitive to further adverse moves.

Theta: At entry, the ZEBRA has little to no net theta because extrinsic value has been neutralized. You are neither collecting time decay as a premium seller would, nor bleeding it as a naked options buyer would. This theta-neutral entry is a core feature of the structure. However, and this is the critical management signal, if the stock moves against you and the long strikes become the at-the-money strikes, the trade can pick up significant negative theta. This is the real danger sign in a ZEBRA, not simply the passage of calendar time.

Vega: The ZEBRA has modest positive vega at entry. A rise in implied volatility will benefit the position slightly, since the long options carry more vega than the short. This is a secondary consideration – the ZEBRA is primarily a directional trade, not a volatility trade – but it is worth knowing when evaluating a position.

Gamma: All three legs of the ZEBRA share the same expiration. The gamma dynamics are therefore not about different expirations but about how the position responds to movement. As the position approaches expiration and the underlying sits near the short strike, gamma behavior becomes more complex. This is one of the reasons managing the position before expiration is important.

How to Set Up a ZEBRA: Step by Step

Step 1: Identify a high-conviction directional view

The ZEBRA is a directional trade. You need a reason to be bullish or bearish – a fundamental thesis, a technical level, a sentiment signal. This is not a neutral strategy and should not be traded without a specific view.

Step 2: Choose the right underlying

The ZEBRA works best on liquid underlyings with tight bid-ask spreads. ETFs like SPY, QQQ, GLD, and IWM are ideal. Individual stocks work but require careful bid-ask accounting. Avoid options chains with wide spreads where the extrinsic offset math gets distorted by market microstructure.

Step 3: Prefer low IV

As established, low IV is the ideal ZEBRA environment. Entering in a high IV environment widens the debit and increases risk without proportionally improving the structure.

Step 4: Select the expiration

tastytrade generally recommends 45 to 60 days to expiration for a standard ZEBRA entry, giving enough time for your directional thesis to develop while keeping liquidity reasonable. Personally, I prefer a much shorter-duration ZEBRA, usually 14 to 21 DTE, and then rolling it. I find this approach more dynamic and capital-efficient.

Step 5: Find the 70-delta and 50-delta strikes

Most platforms allow filtering by delta. The 70-delta ITM strike is your long, the 50-delta ATM strike is your short.

Step 6: Verify the extrinsic math

Before entering, confirm that the extrinsic value of the two long options approximately equals the extrinsic value of the short option. A practical shortcut: look at the OTM option at the same strike as your ITM long, its premium is a rough proxy for the extrinsic value embedded in the ITM long. If two of those approximate the ATM option premium, you have a clean ZEBRA setup.

Step 7: Enter as a single multi-leg order

Never leg in separately. The extrinsic value offset is the entire foundation of the structure. If the underlying moves between fills, the math breaks.

Managing the ZEBRA

Managing a ZEBRA is very different from managing undefined-risk short premium strategies. This difference is important.

The 21 DTE rule does not apply the same way

For undefined-risk positions like short strangles, rolling at 21 DTE collects additional credit and extends the trade favorably. For a ZEBRA, rolling out in time typically costs a debit, which adds to your risk basis. Applying the 21 DTE rule mechanically to a ZEBRA can make a losing position more expensive rather than more manageable.

The real management anchor is when your long strikes become ATM

If the underlying moves against you and your two long ITM options become the at-the-money options, the trade’s character has fundamentally changed. The position is now carrying negative theta, the built-in stop loss is being tested, and continuing to hold may not be the right decision. This is the specific signal for meaningful management point, a structural shift in the position.

Ratcheting winners

When the ZEBRA moves significantly in your favor, you can use the concept of “ratcheting”, securing gains by adjusting the position upward after a profitable move. The practical implementation is to close the existing structure and reopen a new ZEBRA centered around the new, higher stock price. This secures the gain from Phase 1 (the supercharged delta zone). It resets your breakeven at the new price. You can enjoy more upside from the new position without losing your profit if the stock reverses.

Selling short-term options against the longs

Because you hold two long ITM options, you can sell shorter-dated options against them, effectively running a diagonal spread on top of the ZEBRA structure. If the underlying stays range-bound, the short-term premium collected offsets the cost basis of the long legs over time. This does reduce your maximum upside on a sharp move in your favor, so it is a trade-off: income generation in exchange for some cap on the supercharged Phase 1 delta.

ZEBRA vs. LEAPS vs. Synthetic Long

Traders with a strong directional view commonly compare three structures: LEAPS, synthetic long stock, and the ZEBRA.

| 100 Shares | LEAPS (ITM call) | Synthetic Long | Call ZEBRA | |

|---|---|---|---|---|

| Capital required | Full stock price | Moderate | Low (margin) | Low (debit) |

| Maximum loss | Stock price × 100 | Premium paid | Unlimited (put side) | Debit paid |

| Extrinsic drag | None | High | Low | Near zero |

| Starting delta | 100 | 70-80 | ~100 | ~90-100 |

| Upside | Unlimited | Unlimited | Unlimited | Unlimited |

| Ideal IV | Any | Low | Low | Low |

The LEAPS gives you 70 to 80 delta but carries significant extrinsic value – often several hundred dollars per contract – that decays daily regardless of stock movement. The synthetic long gives near-100 delta with minimal premium drag but carries undefined risk on the short put side and requires substantial margin.

The ZEBRA occupies the optimal middle ground for most directional traders: near-100 delta, near-zero extrinsic drag, defined maximum loss, modest capital requirement, unlimited upside. The trade-offs: you need to manage the position actively and the supercharged Phase 1 delta eventually compresses above the short strike, but for a trader with a defined directional conviction and limited capital to deploy, it is one of the most efficient tools in the options toolkit.

When to Use the ZEBRA

High-conviction directional moves. The ZEBRA rewards accuracy. If you have a specific fundamental or technical reason to expect a sustained move, the ZEBRA captures it efficiently.

Low implied volatility environments. As established, low IV makes the debit smaller, the setup cleaner, and the trade more capital-efficient. When IV is elevated, the cost of the long legs rises significantly and the risk-reward shifts.

Capital-constrained accounts. For smaller accounts, the ZEBRA allows meaningful participation in high-quality names (SPY, QQQ, GLD, AAPL) at a fraction of what stock ownership would require.

As a portfolio directional overlay. Rather than carrying outright long stock exposure, the ZEBRA can provide a similar delta footprint with defined maximum loss. This is particularly relevant for traders who run short premium portfolios and want to add directional exposure without unlimited risk.

When you want to participate in a quality stock after a selloff. If a fundamentally sound stock drops on broad market weakness or temporary sentiment, IV may still be at reasonable levels while the stock is at an attractive price. This is often a good ZEBRA setup: low to moderate IV, strong fundamental conviction, stock at or below fair value.

The Put ZEBRA as an Emergency Hedge

This is one of the most practically valuable, and almost never discussed applications of the put ZEBRA, and it comes directly from managing a short premium portfolio during sustained volatility clusters.

During a fast, sustained selloff, buying power can compress in ways that catch even experienced traders off guard. Two forces hit simultaneously: short puts expand in value and inflate margin requirements, while the portfolio drifts long delta as the market falls through short strikes. Most brokers run stress-weighted margin engines that amplify tail-risk scenarios in real time. These forces can destroy a margin buffer in minutes and force involuntary position closes at exactly the worst moment, when premium is richest and closing is most costly.

The instinct in a panic selloff is to buy outright puts. I resist it. At VIX 30 or higher, puts are maximally overpriced. You are paying fear premium on top of fear premium, the worst possible time to be an outright options buyer.

The put ZEBRA solves this precisely, and this is the one context where entering in elevated IV is not only acceptable but intentional. By buying two ITM puts (70 delta) and selling one ATM put (50 delta) with strikes balanced so net extrinsic is near zero, you get a position that behaves like -100 delta, long vega, and long gamma simultaneously. It hedges directional risk, volatility expansion, and convexity all at once, and the ATM put you sell offsets most of the inflated extrinsic embedded in the long puts, so you do not pay the full panic premium that outright put buyers absorb.

Conclusion

The ZEBRA – Zero Extrinsic Back Ratio – offers an innovative approach to stock replacement, and from my personal experience and backtesting results, it is the most effective way to synthetically get long or short I have found. It gives you the same directional exposure as owning 100 shares, with a fraction of the capital, a defined maximum loss, and no extrinsic value drag working against you from the moment you enter.

That last point matters more than most traders realize. Every day you hold a naked call or put, you are fighting time decay. A ZEBRA removes that fight from the start. Your breakeven is roughly the current stock price, your upside is unlimited, and your maximum loss is limited to the debit paid.

For smaller accounts or traders who want to optimize how their capital is deployed across multiple positions, the ZEBRA makes participation in high-quality names genuinely practical. For portfolio managers running short premium strategies, it adds directional or hedging exposure without the undefined risk that can destroy margin during a fast market move.

The OptionsJive Trading Plan covers how I deploy the ZEBRA alongside short premium positions – entry rules, sizing relative to portfolio delta, management triggers, and how it fits into a complete options trading system. If you are serious about adding the ZEBRA to your options trading arsenal, that is the logical next step.

Frequently Asked Questions

What does ZEBRA stand for in options trading?

ZEBRA stands for Zero Extrinsic Back Ratio (or Zero Extrinsic Value Back Ratio). It refers to the fact that the strategy is constructed as a back ratio spread where the net extrinsic value of the position is approximately zero.

Who created the ZEBRA options strategy?

The ZEBRA strategy was coined and popularized by Liz Dierking and Jenny Andrews on their tastytrade show Calling All Millionaires.

Is the upside on a ZEBRA capped?

No. The ZEBRA has all of the upside profit potential of owning stock. Above the short strike, the position’s delta compresses back toward 100, but the upside continues to be unlimited. The position still profits dollar-for-dollar with the underlying above the short strike, it just loses the supercharged delta it had between the two strikes.

What is the maximum loss on a ZEBRA trade?

The maximum loss is the net debit paid to enter the position. Unlike owning stock (where losses can be very large) or short stock (unlimited losses), the ZEBRA has a defined worst-case.

When should I manage or close a ZEBRA position?

The primary management signal is structural, not calendar-based. When your long strikes become the at-the-money strikes, meaning the stock has moved significantly against you, the trade has changed character and negative theta has entered the position. That is the key management trigger. Unlike undefined-risk strategies, rolling a ZEBRA at 21 DTE typically costs a debit and may add risk rather than reduce it.

What is the ideal implied volatility environment for a ZEBRA?

Low implied volatility is the ideal setup condition for both call and put ZEBRAs. Lower IV means cheaper long options, a smaller net debit, and a cleaner extrinsic offset.

Can I use the ZEBRA in an IRA?

Yes. Liz and Jenny specifically highlighted the ZEBRA’s suitability for IRA accounts, where naked short stock or certain undefined-risk structures are not permitted. Because the ZEBRA has defined maximum loss equal to the debit paid, it is compatible with IRA account restrictions at most brokerages.

What is ratcheting a ZEBRA?

Ratcheting refers to closing a profitable ZEBRA and reopening a new one centered at the new, higher stock price after a significant upward move. It locks in the gain from the initial position and resets the structure, same defined risk, same unlimited upside, but now starting from a higher base.