I’ve been trading options for a long time, and the 1-1-2 is still the structure I find myself coming back to more than any other. Not because it wins every time (it doesn’t) but because its risk profile is genuinely unusual. It collects premium in flat and rising markets. It generates more profit in a moderate selloff. The only scenario where it causes real pain is a fast, deep collapse, and even then the damage is a function of position sizing, not the strategy itself. That combination of properties is rare in options trading, and once you understand how the structure works, it’s hard to look at a plain short strangle or iron condor the same way again.

How the 112 Options Strategy Works

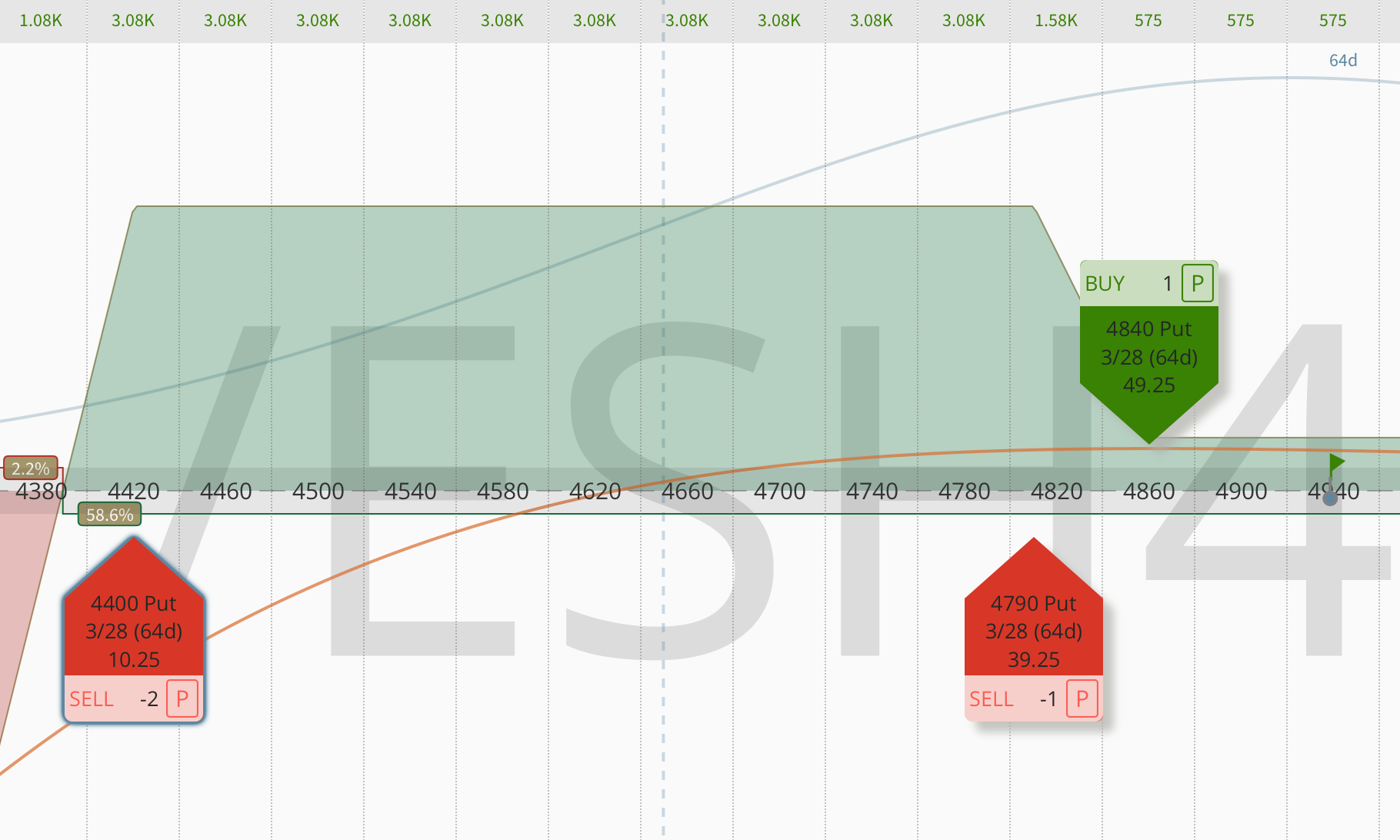

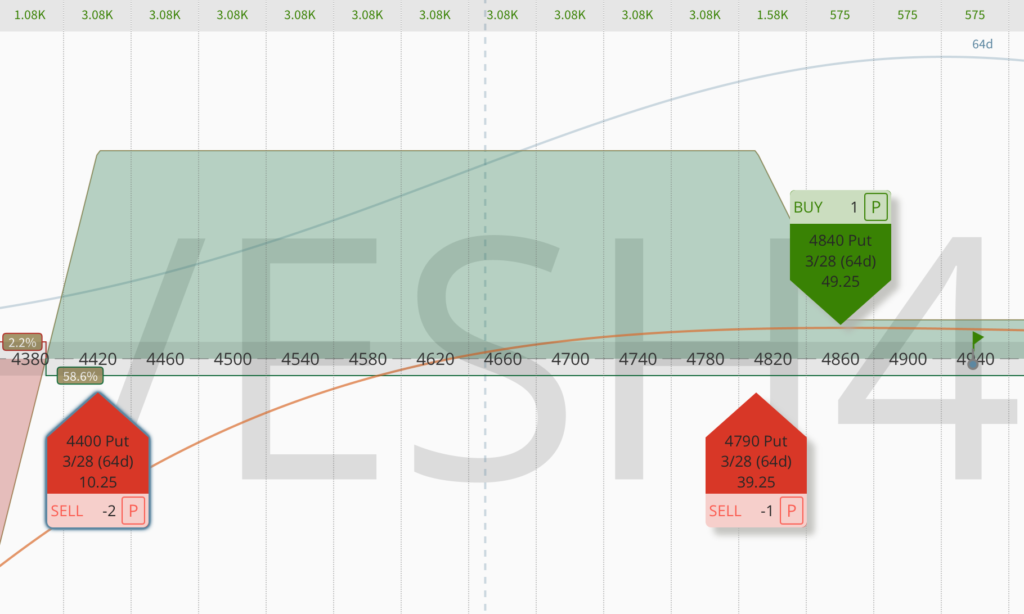

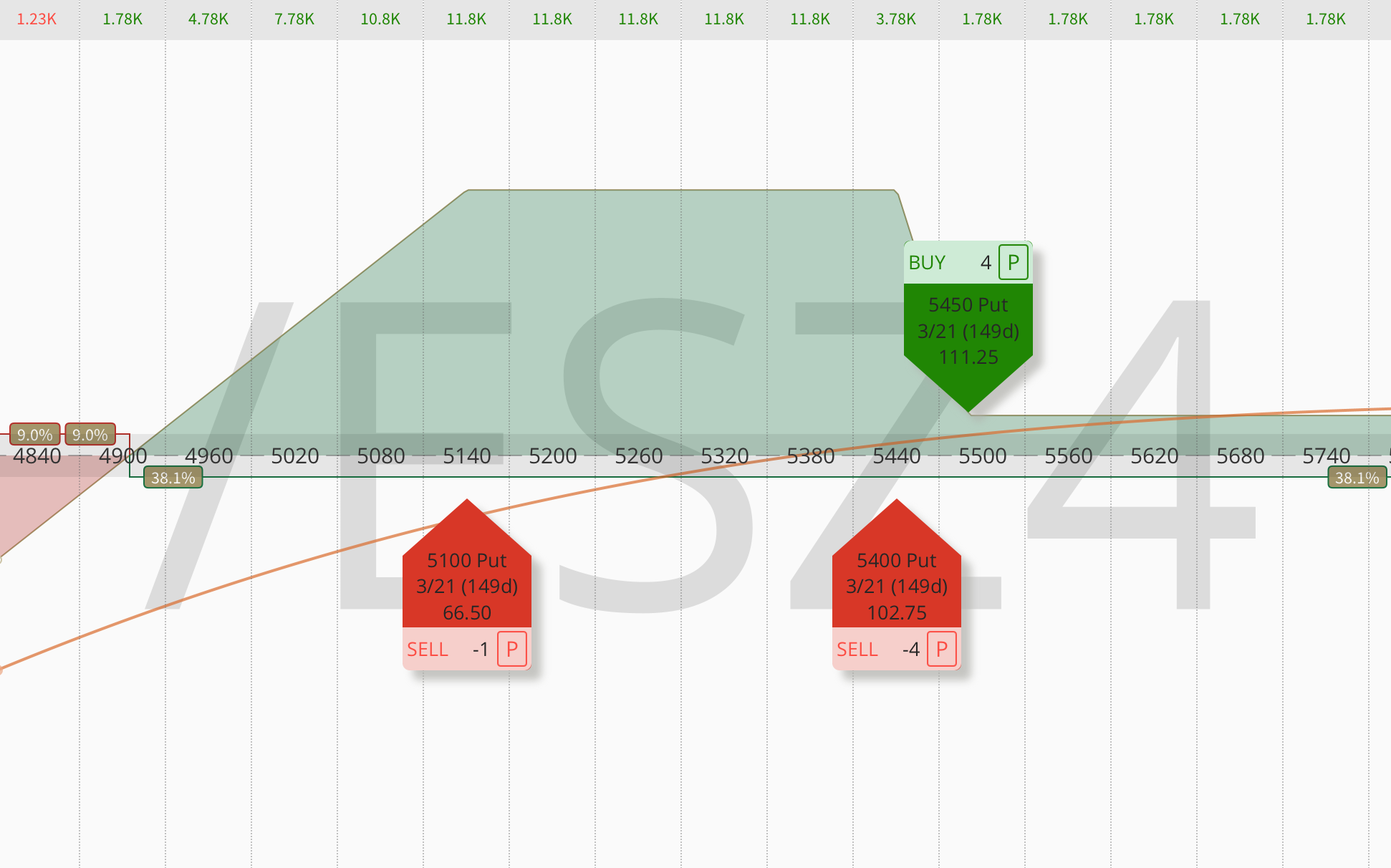

The 1-1-2, also called the bear trap or the 112 put ratio, is a three-part structure built entirely with puts. You buy one put, sell one put closer to the money to form a debit spread, and sell two additional puts much further below. In delta terms: long the 25-delta put, short the 20-delta put, short two puts at around the 5 delta.

The debit spread costs a small debit. The two far-OTM naked puts collect approximately double that cost, leaving the entire position at a net credit. On a typical /ES trade, that credit lands around $10-12 per contract, roughly $550 collected on $6,500 in buying power.

The name reflects the leg count: one long put, one short put, two far-OTM short puts. Three options, one structure.

Zero Upside Risk

The first thing worth understanding about the 1-1-2 is that it carries zero upside risk. If the market rallies, all three legs expire worthless and you keep the net credit in full. There is nothing to worry about above your entry point.

This makes the 1-1-2 fundamentally different from most neutral strategies. An iron condor gets hurt when the market makes a strong move in either direction. The 1-1-2 doesn’t care about upside at all, it sits below the market, collecting premium, while time works in its favor.

Two Ways to Win

Here’s what I find genuinely fascinating about this structure, and the reason I keep coming back to it. The 1-1-2 has two completely different profit scenarios that work through opposite mechanisms. I call them the tail and the trap.

The tail is what most people see first. The market stays flat or rallies, all three options decay toward zero, and you collect the net credit. Theta does the work, you close the position and move on.

The trap is the interesting one. If the market sells off moderately, enough to push the underlying down toward the debit spread, but not far enough to breach the two naked puts below, the debit spread starts appreciating rapidly. The two naked puts far below are still safe. You collect the credit plus the maximum profit on the debit spread. The moderate selloff that would hurt a short strangle or iron condor actually increases your total profit.

That’s the Bear Trap. The market drops, sellers feel vindicated, and you make more money than if it had stayed flat. It’s a counterintuitive result that rewards moderate volatility on the downside rather than punishing it.

Why the 1-1-2 Trade?

- Simple mechanical execution

- No need for complex technical or fundamental analysis

- Scalable for different account sizes

- Demonstrates an impressively high success rate

- Zero risk to the upside

- Offers larger payouts in case of an underlying move lower

- Multiple paths to success and exit strategies

How I Set It Up on Futures

My preferred underlying for the 1-1-2 is futures, specifically /ES, /GC, /NG, /CL, and grains like /ZC and /ZW. The reason is liquidity and margin efficiency. SPAN margin on futures allows you to run this structure at a much better capital-to-premium ratio than you’d get on equity ETFs, and the options markets on liquid futures tend to have cleaner put skew to exploit.

On /ES, I enter 45-60 days before expiration, long enough that the naked puts can sit at a comfortable distance from current price, but not so far out that the structure becomes vulnerable to a slow grind lower. For the debit spread, I buy the 25-delta put and sell the 20-delta put, targeting a spread wide enough to cost $7-8 in debit. For the two naked puts, I start at the 5-delta level, collecting $10-11 in credit, roughly double the cost of the debit spread. The net result is $10-12 credit per contract, around $550 collected on $6,500 in buying power.

One important distinction worth understanding before running this on other futures: /ES options are European-style, which means there’s no risk of early exercise and no futures assignment to manage. That’s one reason I lean on /ES specifically for this structure. Options on commodity futures (/GC, /NG, /CL, grains) can be exercised into the underlying futures contract, so if a naked put lands in the money near expiration, you may end up holding a futures position rather than settling in cash. It doesn’t break the strategy, but it changes how carefully you need to manage the final days of the trade in those underlyings.

My optimal 1-1-2 trade example on E-mini S&P 500 futures (/ES):

- The put debit spread (1-1):

- Start at 25 delta for the long put

- Buy the 50 wide spread for $7-8 debit

- Far OTM naked puts (2):

- Start at 5 delta, looking for $10-11 credit

- Collect $10-12cr – $550 on $6,500 in buying power

The Risk You Cannot Ignore

I want to be direct about this, because the 1-1-2 is the kind of strategy that can create a false sense of security during a long winning streak, but the tail risk is real. The two naked puts sitting far below the market are your vulnerability. If the market collapses, if you get a VIX spike to 40, 50, or 60, those naked puts can go from 5 delta to deep in the money faster than you can adjust. On paper, the structure has defined risk on the upside and limited room to manage on the downside when the move is extreme.

Size it so that a worst-case scenario on the naked puts is painful but survivable. I allocate a small percentage of total buying power to any single position and run a diversified book across different underlyings. If /ES gets hit hard, /GC and /ZN often behave differently. Non-correlation is your real hedge, more than any adjustment you can make after the fact.

The 1-1-2 is also negative vega, which means an immediate spike in implied volatility will mark the position against you even before price moves cause damage. SPAN margins can swing dramatically in a fast market, and if you’re already running large, buying power expansion can force your hand at exactly the wrong moment. Know your numbers before you enter, not after.

Managing the Trade

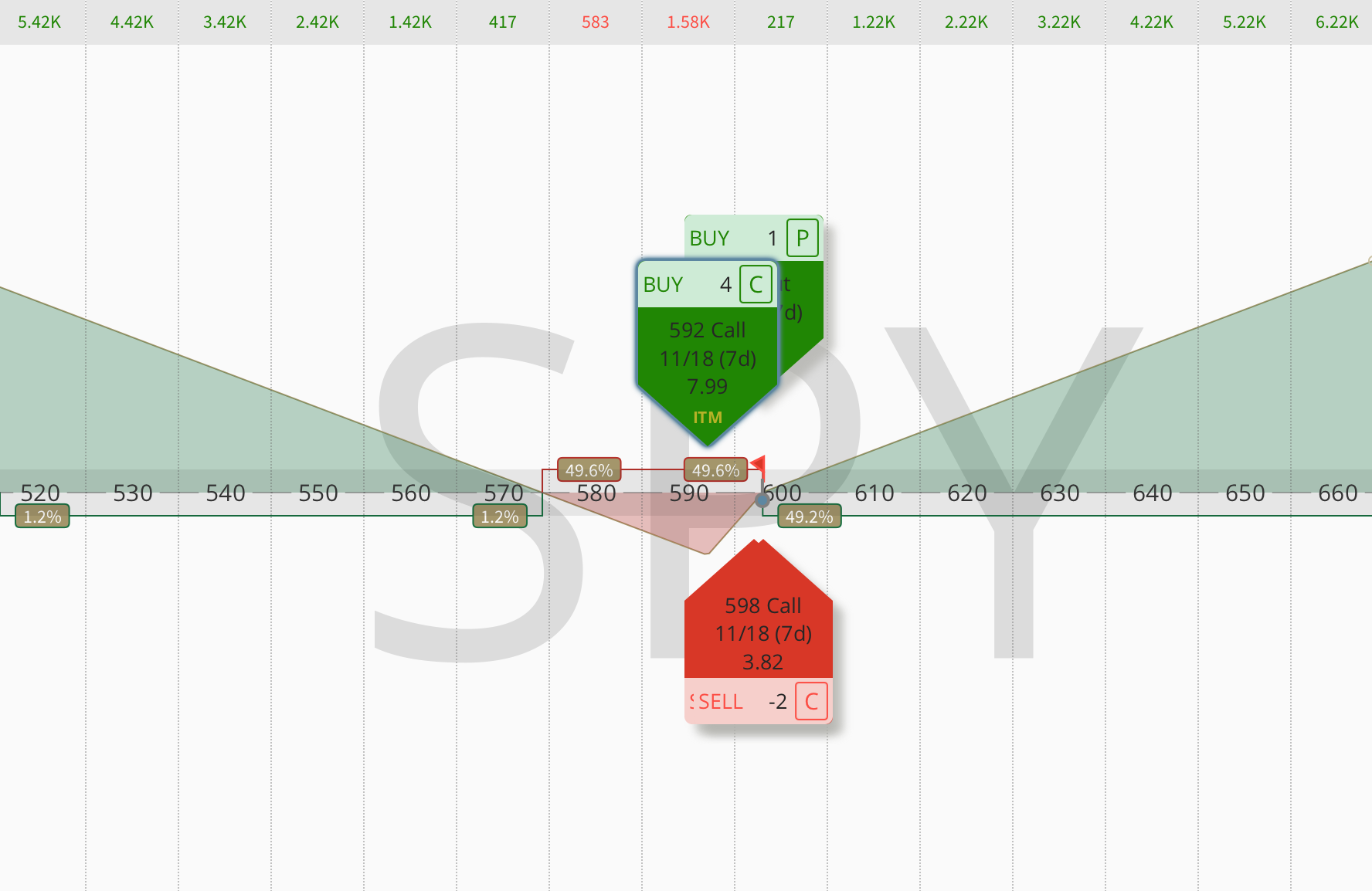

I close the naked puts when they reach 95% of their maximum profit. At that point you’ve collected nearly all the premium they were going to generate, and the residual risk isn’t worth carrying. What you’re left with is the debit spread, which you’ve now acquired for essentially nothing. That spread, sitting below the market at zero cost, becomes a free hedge. If the market ever collapses from that point forward, it pays off. You’re holding a lottery ticket you didn’t have to pay for.

During strong market rallies, I’ve occasionally been able to close the entire 1-1-2 early for an additional credit. The position’s profit curve moves favorably enough, fast enough, that exiting before expiration captures most of the theoretical maximum profit while removing all remaining risk. It doesn’t happen every trade, but when you see that opportunity, take it. Don’t get attached to the remaining theta.

For deeper selloffs where the naked puts come under pressure, the management playbook is more involved: rolling, adjusting strikes, hedging with the Black Swan structure. I’ve written about that in detail in my previous article, which covers the exact steps I take when a position moves against me.

Why I Keep Trading It

The 1-1-2 isn’t a strategy for every situation or every trader. It requires genuine comfort with naked put risk, disciplined position sizing, and the patience to let time do the work. But for traders who have that discipline, it offers something most strategies don’t: a structure that actively benefits from the kind of moderate market volatility that makes most premium sellers uncomfortable. The trap scenario is genuinely unusual, and it’s the reason I keep this trade in permanent rotation.

The 1-1-2 Bear Trap is also one of the core positions inside the official OptionsJive Trading Plan. If you want to see the exact entry rules, sizing guidelines, and the full adjustment playbook for when markets move against you, download the Trading Plan here.

How are you running your S&P 112 campaign? I’ve conducted extensive backtesting and discovered that 120 DTE, 50% PT, and 2x loss (300% value) hit the sweet spot.

After additional backtesting, it appears that managing the PDS separately at 95% profit from the naked puts (50% PT and 200% SL) yielded much better statistics!

Went from being up 7.5% YTD to being down 16% YTD all because of my size. Had too many units and wasn’t prepared for VIX hitting 60 today!