Traditionally, neutral strategies such as the strangle or iron condor carry inherent risks on both sides of the market. A substantial move in either direction can be challenging. You’re selling a put spread and a call spread, collecting premium on both sides, and somewhere in the back of your mind you know that the put side is doing most of the heavy lifting.

The put premium is fat because the market prices downside fear into every OTM put. The call spread? It’s there mostly for symmetry. You’re collecting a fraction of what the put brings in, and meanwhile you’re spending your real money on a long put to define the downside, paying elevated implied volatility for the protection you need most. That tension is exactly what the Jade Lizard was built to resolve.

Why Volatility Skew Changes Everything

To understand why the Jade Lizard works, you need to spend a minute on volatility skew, because once you see it, you can’t unsee it.

In most underlyings, implied volatility isn’t flat across all strikes. It slopes. OTM puts carry higher implied volatility than OTM calls at equivalent distances from the current price. The market perpetually prices in more fear of a sharp drop than a sharp rally. Institutions buy OTM puts constantly as portfolio insurance, which drives their premiums up. OTM calls don’t get the same demand, so they stay relatively cheap.

This has a real consequence for how you collect premium. When you sell a strangle (a naked put and a naked call), you’re not collecting equal money on both sides, the put is your engine. The call is just along for the ride. And when you build an iron condor, you’re buying protection on both sides, which means you’re buying a long put on the expensive side of the skew while buying a long call on the cheap side. You’re paying the most for the protection that costs the most.

The Jade Lizard asks a simple question: what if we stopped being symmetrical about this? Keep the put naked, capture that full skew premium, define only the upside, and size the trade so that the total credit you collect exceeds the width of the call spread. Do that one thing, and you’ve structured a position where no matter what happens to the upside, you cannot lose money there.

The Jade Lizard Setup

The Jade Lizard has three legs: a short OTM put, a short OTM call, and a long OTM call sitting above it. The short call and long call together form a call spread that caps your upside exposure. The put sits on its own, naked, collecting the bulk of the premium.

The critical condition, and this is the entire strategy in one sentence, is that the total credit you collect must be greater than the width of the call spread. That single rule is what creates the no-upside-risk property.

The math is straightforward: say you sell a $5-wide call spread and collect $2.10 from it. You also sell a put for $3.20. Total credit: $5.30. If the stock rallies hard and your call spread goes to maximum loss at expiration, that $5.00 loss is fully absorbed by the $5.30 you already collected. You come out slightly ahead on the upside no matter what.

The only real risk lives on the short put, but that’s the trade-off: more premium, defined upside, undefined downside. It sits between an iron condor and a strangle on the risk spectrum; more premium than the condor, less than the naked strangle, with the upside structurally handled.

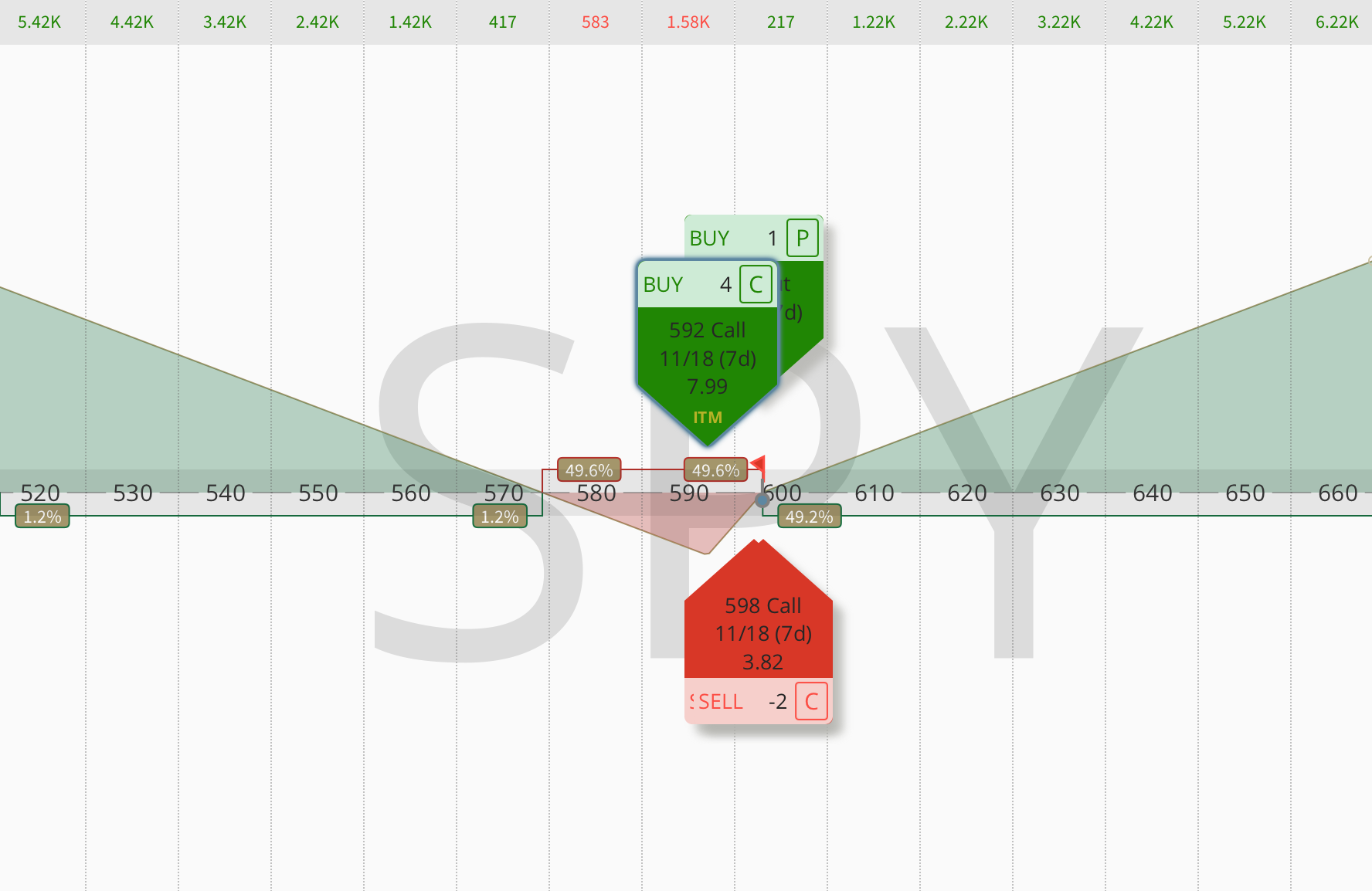

My Real Trade: Boeing

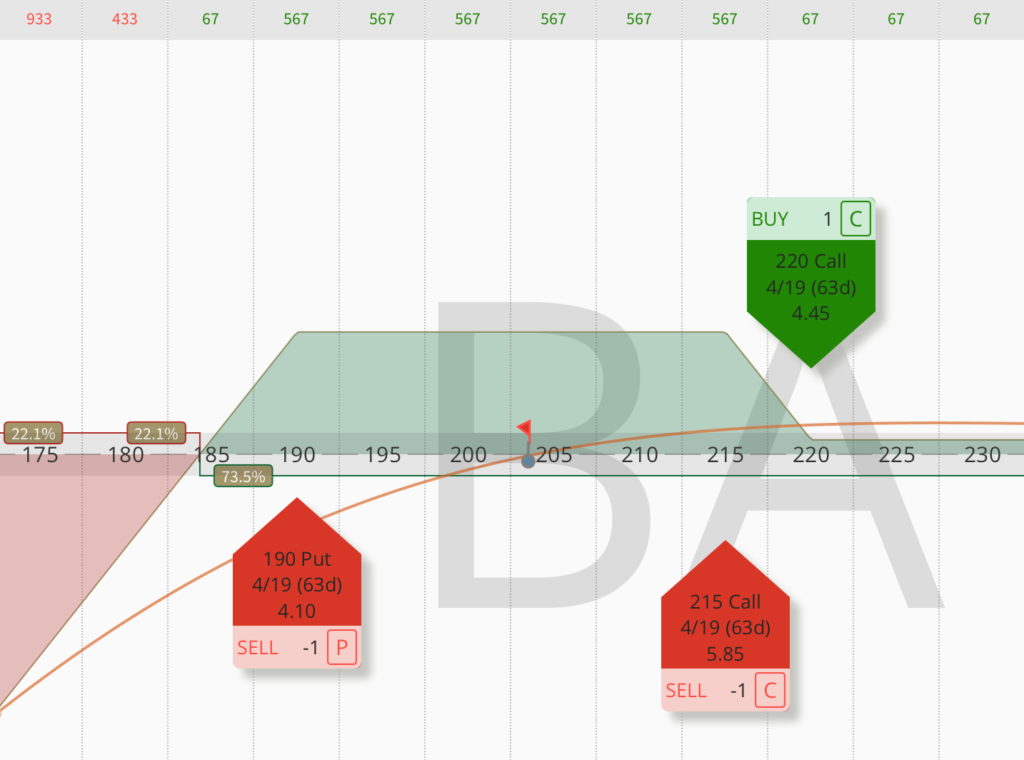

Let me make this concrete. A while back I was looking at Boeing (BA) with an IV rank sitting at 44%. Elevated, after a rough patch of news that had pushed implied volatility higher across the board. With Boeing trading around $200, I set up the following:

Sell the 190 put with April expiration (63 days out) for $4.10. Sell the 215 call and buy the 220 call (a $5-wide call spread) for $1.40 credit. Total credit: $5.50. Call spread width: $5.00. Upside risk: zero.

The position entered with an 80% probability of profit and a downside break-even just under $185. Buying power tied up was around $2,900, mostly from the naked put margin.

What made this trade appealing wasn’t just the structure. Boeing had sold off on genuine uncertainty. Put skew was elevated because fear was elevated. That’s the ideal environment for a Jade Lizard: a company the market has temporarily punished, with put premiums inflated by fear you believe is overdone. You’re not just mechanically selling premium, you’re making a judgment that the fear is excessive, and getting paid well for that judgment.

I wouldn’t run this trade on a stock I didn’t want to own. The naked put means assignment is real. My personal rule is: if I wouldn’t want 100 shares of it at that strike price, I won’t sell the put naked, period. The Jade Lizard isn’t a structure that works around bad stock selection. It assumes you’ve done that work first.

How to Manage a Jade Lizard

Most of the time, nothing dramatic happens, the stock stays in range, theta does its job, and I close the position at 50% of the maximum credit. That’s my standard target: take half the premium off the table early, remove most of the remaining risk, move on. Waiting for expiration to squeeze out the last dollar of premium rarely makes sense. You’ve already earned most of the edge.

If the stock rallies strongly, don’t stress. That’s the point of the structure, the call spread going against me can’t exceed the total credit I collected. If I want to actively improve the position, I can roll the short put strike upward toward current price to collect additional credit and bring the downside break-even closer in. But there’s no urgency. The upside is already handled.

The more interesting scenario is a selloff. If the underlying drops toward the short put, the instinctive move is to roll the put down and out in time for a credit, extend duration, give the trade more room. That works, but my preferred approach is actually to roll the call spread down toward current price instead. This collects additional credit and improves the downside break-even without touching the naked put at all. It’s a cleaner adjustment because you’re not worsening your break-even prices on the side that’s already under pressure.

The Jade Lizard vs. The Strangle

One question I get often is why not just trade a strangle instead. The strangle is simpler: sell a put, sell a call, no call spread needed, more premium all around.

The answer is the long call. Adding it costs a small debit but structurally eliminates the upside risk. For a lot of traders, and for me, especially on single-stock positions, that matters. Stock prices can make violent moves to the upside around earnings, acquisitions, or short squeezes. The Jade Lizard keeps you in the trade through that kind of move. A naked strangle can turn a manageable situation into an emergency very quickly.

In a low-skew environment where put and call implied volatilities are roughly equal, the strangle often wins on pure premium. In the typical high-skew environment, which is most of the time in most underlyings, the Jade Lizard captures the skew advantage on the put side while handling the side of the trade that’s most vulnerable to a sudden shock.

When It All Fits Together

The Jade Lizard isn’t a strategy I use on every trade; it earns its place when IV rank is elevated enough to generate meaningful put premium, when I have a neutral to slightly bullish outlook on an underlying I’d actually want to own, and when the put skew is fat enough to make the naked put worth the exposure.

When those three things line up, particularly after a selloff in a quality name, the Jade Lizard is one of the most elegant tools in options trading. You’re collecting rich premium, you’ve eliminated the risk on the side that’s historically less dangerous, and you’ve structured a position that makes rational sense both mechanically and fundamentally. That’s the iron condor’s smarter sibling. The Jade Lizard is also one of the core positions inside the OptionsJive Trading Plan.

How did Jade Lizards perform in the past compared to the naked put?