Most investment portfolios share a fundamental limitation: they only make money when the market goes up. Stocks, ETFs, long calls – they all require upward movement to generate returns. When the market grinds sideways or trades in a tight range, traditional investments simply sit there. The iron condor options strategy was designed to profit specifically from that environment: from range-bound markets, from time decay, and from declining implied volatility.

It sounds like the ideal income machine. In the right conditions, traded correctly, it is. But the track record of passive iron condor trading tells a very different story, and if you understand why, you will understand exactly when and how to use this strategy in a way that actually works.

What Is an Iron Condor?

An iron condor combines two credit spreads into a single four-leg position: a put credit spread below the current price and a call credit spread above it, both in the same expiration.

The four legs:

- Sell an OTM put (short put – inner strike)

- Buy a further OTM put (long put – the lower wing)

- Sell an OTM call (short call – inner strike)

- Buy a further OTM call (long call – the upper wing)

The two short options form the body. The two long options define your maximum loss. You collect a net credit at entry. That credit is your maximum profit, realized when the underlying expires anywhere between your two short strikes and all four options expire worthless.

Think of it as selling a short strangle (a short OTM put and short OTM call) and buying protective insurance on both sides. The wings cost some of the premium you collected, reducing your max profit, but they cap what you can lose if the underlying makes a large move.

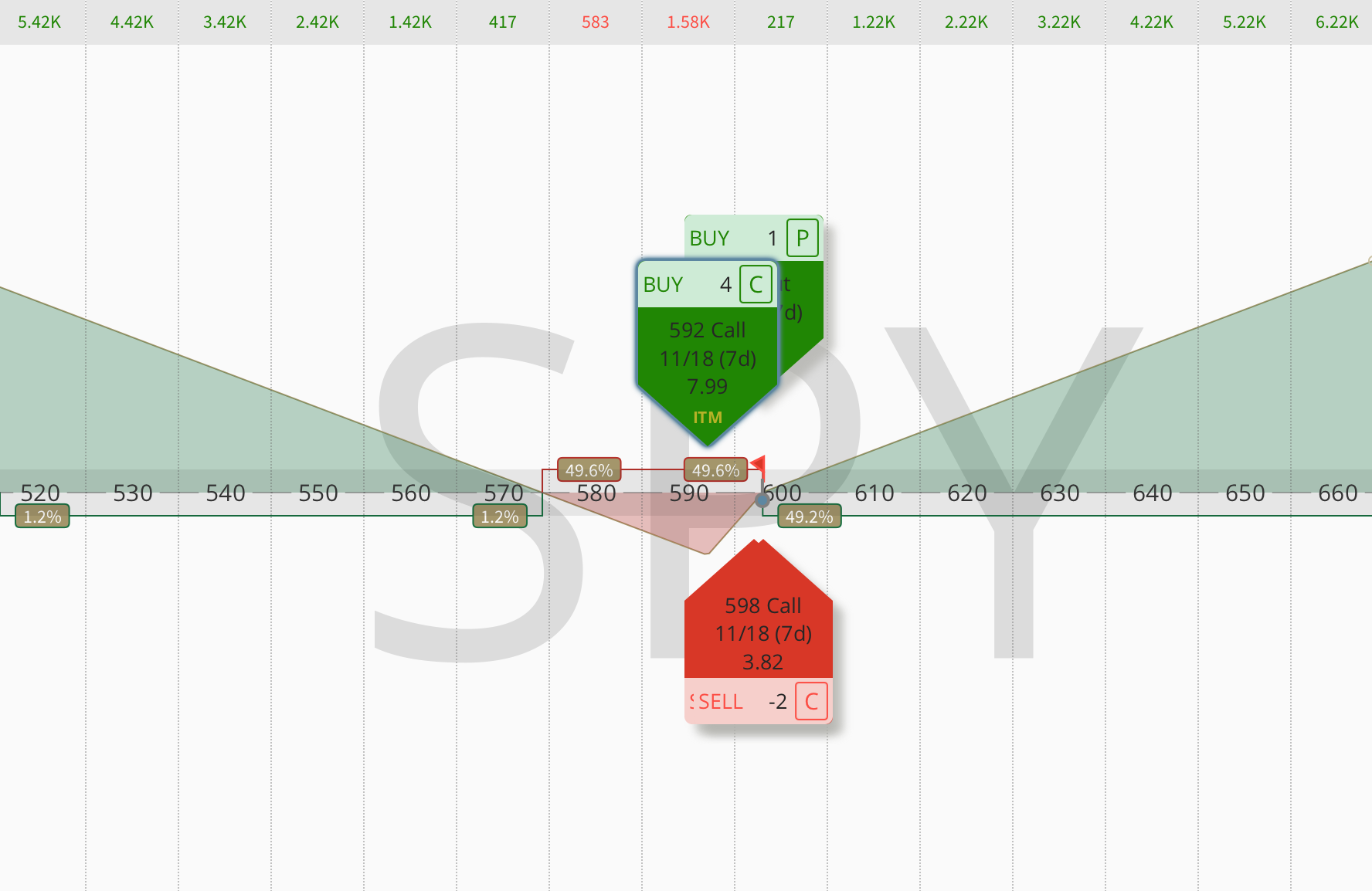

A concrete example. SPX at 5,200:

| Leg | Strike | Action | Premium |

|---|---|---|---|

| Short put | 5,050 | Sell | +$2.50 |

| Long put | 5,040 | Buy | -$0.80 |

| Short call | 5,350 | Sell | +$2.50 |

| Long call | 5,360 | Buy | -$0.80 |

| Net credit | $3.40 |

The full credit is kept when SPX expires between the two short strikes (between 5,050 and 5,350). The breakevens, where the position moves from profit to loss, sit at 5,046.60 on the downside and 5,353.40 on the upside. As long as SPX stays within that wider range at expiration, the trade is profitable.

Is the Iron Condor Strategy Dead?

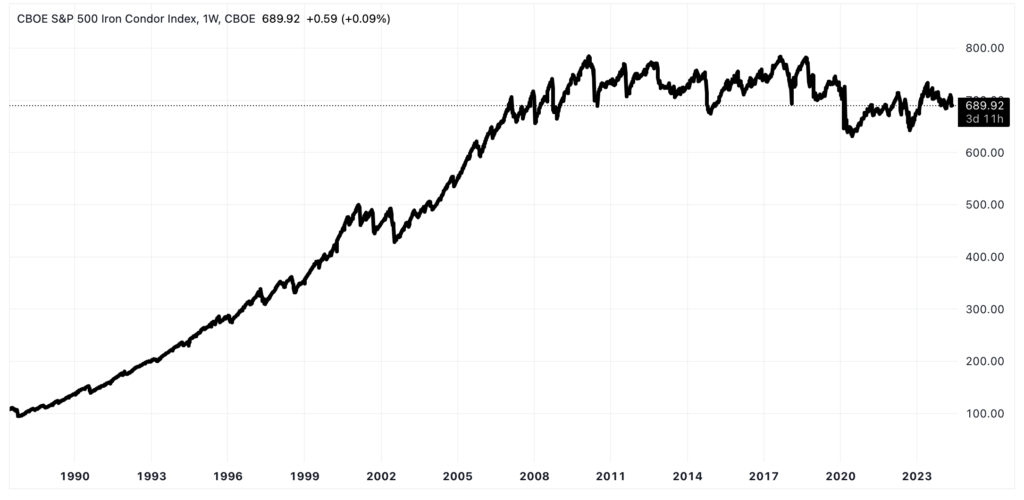

The most honest way to evaluate any options strategy is to look at what a passive, mechanical version of it actually produced over time. For iron condors, that benchmark exists. The CBOE S&P 500 Iron Condor Index (CNDR) tracks the hypothetical performance of a monthly SPX iron condor; selling short options at approximately 20 deltas, buying long options at approximately 5 deltas, no adjustments, no management, mechanical monthly roll.

The data divides into two very different eras.

January 1987 to January 2010: Compound annual growth rate of +9.11%. The strategy appeared to work. Traders who ran a passive iron condor on the S&P 500 were generating meaningful returns.

January 2010 through 2024: The index moved from 770 to approximately 784 – essentially flat for 14 years. Compound annual return for that period: approximately -0.72%. The full 37-year CAGR: 5.28%.

Compare that to a simple buy-and-hold of the S&P 500 over the same 37-year period, which delivered approximately 10.5% annualized. The passive iron condor underperformed by nearly half.

Is the iron condor strategy dead? This data makes one thing unmistakably clear: the passive, set-and-forget version is dead. The CNDR uses fixed deltas, makes no adjustments, and enters every month regardless of the volatility environment. It is the worst possible version of the strategy, and 14 years of near-zero returns show exactly what that gets you.

The strategy itself is not broken. The approach is.

Why Passive Iron Condors Underperform

Two structural forces explain the CNDR’s underperformance since 2010. These forces are crucial for understanding how to trade iron condors effectively.

Low volatility compresses premium. Iron condors are short volatility trades; you profit as implied volatility contracts and options lose value. When you enter in a low IV environment, you are selling options that are already cheap. The credit is thin, the wings cost proportionally more, and the net risk-reward deteriorates. The post-2010 era has been characterized by persistently suppressed volatility relative to historical averages, punctuated by brief spikes. A mechanical iron condor entered every month regardless of IV level collected inadequate premium in most cycles.

Sustained trends create systematic breaches. Iron condors require range-bound markets. The S&P 500 from 2010 to 2024 was in one of the strongest sustained bull markets in history. A mechanical call-side short strike placed at 20 delta gets hit when the market relentlessly grinds higher month after month. The strategy has no ability to adapt, and the losses on the call side eroded all the gains from quieter months.

The lesson is that iron condors require two important inputs that the CNDR ignores: volatility regime filtering and active management. Without both, you are fighting the market rather than harvesting from it.

Iron Condor vs. Short Strangle

The iron condor is, structurally, a short strangle with wings. That relationship matters because it clarifies exactly what you gain and what you sacrifice by choosing one over the other.

A short strangle (selling a naked OTM call and put) collects more premium, carries a higher probability of profit (typically around 70% at 16-delta strikes), and benefits more from volatility contraction because the position has no long options diluting its vega. The trade-off is undefined risk. A big move, especially overnight or over a weekend, can lead to losses greater than what the position seemed to risk when you entered.

An iron condor sacrifices some edge in exchange for defined risk. The wings reduce buying power requirements, cap maximum loss, and smooth out P&L swings. The trade-off: lower premium, lower probability of profit (typically around 60%), and reduced vega sensitivity.

| Factor | Short Strangle | Iron Condor |

|---|---|---|

| Maximum loss | Undefined | Defined (spread width – credit) |

| Probability of profit | ~70% at 16 delta | ~60% at 16 delta |

| Premium collected | Higher | Lower |

| Vega sensitivity | More negative | Less negative |

| Buying power used | Higher | Lower |

| Suitable for IRAs | No | Yes |

tastylive’s research has consistently found that undefined risk strategies outperform defined risk strategies on an expected value basis. The wings are negative expected value insurance; you pay for them, and on average you overpay. However, for IRA accounts where naked options are prohibited, or for traders who need the psychological certainty of a known maximum loss, the iron condor is the appropriate tool. Strangles are better on paper for potential gains. Iron condors are easier to manage for many traders.

My Entry and Management Rules

Here are the key rules I follow. They set smart iron condor trading apart from the passive method, which leads to 14 years of nearly zero returns.

Rule 1: Trade Highly Liquid Underlyings Only

Liquidity is not a preference on iron condors. You have four bid-ask spreads working against you on entry and four more on exit. For a strategy that depends on collecting a specific net credit, wide spreads directly eat your edge before the trade even begins. Stick to SPX, SPY, QQQ, and IWM – liquid index underlyings where markets are tight and deep. Individual stocks require careful attention to options chain liquidity.

Rule 2: Enter When Implied Volatility Is Elevated

This is the single most important filter and the one that explains most of the CNDR’s underperformance since 2010.

Iron condors are short volatility trades. Entering when IV is low means selling options that are already cheap, collecting inadequate premium for the risk taken, and having little room for mean reversion to work in your favor. Entering when IV Rank is above 35 means selling options that are overpriced relative to what the market is statistically likely to do. That is where the edge lives.

The tastylive SPY Iron Condor study demonstrated the impact precisely. A passive iron condor held to expiration at any IV level produced a 53% win rate, barely above the theoretical 50/50. The same structure managed at 50% profit target produced 62%. Filtered specifically for IVR above 35 at entry, combined with active management: 70% win rate. Same structure, same underlying, dramatically different outcomes based on when you entered.

Additionally, avoid entering during strong trends. Iron condors profit from neutral markets. A market trending decisively in one direction will breach the spread on one side and punish you for placing a neutral trade in a directional environment.

Rule 3: Strike Selection and the 1/3 Width Rule

Target 16-delta options on both short strikes. At 16 delta, the option has approximately an 84% probability of expiring worthless; a strong structural starting point.

For premium: collect at least 1/3 of the spread width in net credit. On $5-wide spreads, that means at least $1.67. On $10-wide spreads, at least $3.33. This rule ensures the risk-reward is acceptable before you enter. Iron condors that collect less than 1/3 of width are structurally unfavorable and should be passed. The credit you collect is your maximum profit; if it is too small relative to your maximum loss, no amount of management rescues the trade.

Rule 4: Optimal Expiration – 45 to 75 DTE

Target 45 to 60 days to expiration. This window sits in the zone where theta decay is efficient but gamma risk is not yet dangerous. The theta decay curve accelerates meaningfully in this range while the position is still far enough from expiration to absorb moderate moves without immediate crisis.

Avoid expirations below 30 DTE – the gamma risk accelerates too fast and small moves create large P&L swings. Avoid expirations beyond 75 DTE – the capital is tied up too long relative to the premium collected and vega exposure becomes too dominant.

Rule 5: Close at 25-50% of Maximum Profit

Do not hold iron condors to expiration. Close when you have captured 25-50% of your maximum profit.

At that point, you have collected the majority of the available theta. The short strikes are likely still comfortably out of the money. Continuing to hold means accepting full gamma risk – the dangerous final-week zone where the position becomes highly sensitive to sudden moves – for the small remaining gain. It is a poor exchange: significant additional risk for diminishing additional reward.

My mechanical rule: when the position can be bought back for 50-75% of what you collected, close it. Take the profit, free the capital, redeploy it in a new position if the conditions still warrant it.

Rule 6: Manage the Untested Side When Tested

When the underlying approaches one of your short strikes, the standard adjustment is to roll the untested side (the spread that has room to move) closer to the current price. This collects additional premium, reduces your cost basis, and brings the position back toward delta-neutral.

Do not roll the tested side. That would increase your directional exposure into the move that is already working against you. Roll the side with room, and collect credit for doing it.

If the underlying moves decisively through a short strike and the spread approaches maximum loss, the decision is whether to take the loss cleanly or roll the entire position out in time for a credit. Rolling buys more time but extends your commitment to the trade. Make that decision based on whether your original thesis is still credible. If the market is in a strong trend, rolling is stubbornness, not management.

Iron Condor vs. Iron Butterfly

The iron butterfly is the compressed version of the iron condor; both short strikes are placed at the same ATM strike. This generates significantly more premium because ATM options carry maximum extrinsic value. The trade-off is a much narrower profit window: the iron butterfly profits when the underlying expires very close to the short strike, whereas the iron condor has a wider profit zone between the two short strikes.

For most traders in most environments, the iron condor is the more practical choice. The iron butterfly is appropriate when IV is exceptionally high and the underlying is expected to stay tightly pinned, when you want maximum premium for a narrow outcome. The iron condor is the right choice when you want a wider zone of success with less sensitivity to the exact expiration price.

Position Sizing: The Most Underestimated Risk

The defined risk label creates a false sense of safety that leads to oversizing, which is one of the most common and costly mistakes in iron condor trading.

The maximum loss on a 10-wide iron condor might be $700. On 50 contracts of the same trade, it is $35,000. “Defined risk” only protects you if the position is sized so that the maximum loss is survivable and proportional to the account.

Guideline: risk no more than 2-5% of net liquidation value on any single iron condor position. At this sizing, even a maximum loss on a single trade is manageable and does not threaten the portfolio’s ability to continue operating.

The second sizing consideration is correlation. Iron condors on SPY, QQQ, and SPX within the same account are not independent positions, they will all move together in a market dislocation. True diversification means trading iron condors across genuinely uncorrelated underlyings.

Conclusion

The iron condor is not dead. The passive version is.

By following the rules above – entering when implied volatility is elevated, going wider than feels comfortable, closing at 25-50% of max profit, and adjusting the untested side when tested – you can master the iron condor strategy and make it work in your favor. Remember that practice and patience are key. No strategy produces results overnight, and iron condors require you to trade through losing months without abandoning your process.

Trading market-neutral iron condors can be very profitable and add much-needed diversification to any investor’s portfolio, particularly for accounts that cannot run undefined-risk strategies. Used correctly, the iron condor generates income in conditions where most strategies simply wait.

The difference between the CNDR’s 14 years of flat returns and a disciplined, actively managed iron condor approach is filters, sizing, and the willingness to manage positions rather than hope they expire in your favor.

The OptionsJive Trading Plan includes iron condors as part of a full system. It explains when to choose them over short strangles, how to size them in a portfolio, and the entry and exit rules I use.

Frequently Asked Questions

Is the iron condor strategy still profitable?

Yes, but not in its passive form. 14 years of CBOE CNDR data show that a mechanical, unadjusted iron condor on SPX delivered near-zero returns from 2010 to 2024. Actively managed iron condors, entered in elevated IV environments and closed at 50% of max profit, have consistently shown win rates of 60-70% in tastylive research.

What is the best IV environment for iron condors?

IVR above 35, ideally above 50. Iron condors are short volatility trades; they need elevated implied volatility to generate adequate premium and to benefit from mean reversion as IV contracts.

When should I close an iron condor?

At 25-50% of maximum profit. Do not hold to expiration; the gamma risk in the final weeks can turn a profitable position into a loss for a small remaining gain.

How do I adjust an iron condor when tested?

Roll the untested side closer to the current price to collect additional premium and rebalance delta. Do not roll the tested side.

Iron condor vs. short strangle – which is better?

Short strangles collect more premium and have higher probability of profit, but carry undefined risk. Iron condors have lower premium and probability but defined maximum loss and lower buying power requirements. Tastylive research shows that undefined risk strategies offer higher expected value. However, iron condors are better for IRA accounts and traders who need defined risk.

What strikes should I choose for an iron condor?

Target 16-delta options on both short strikes and aim to collect at least 1/3 of the spread width in net credit. Below 1/3 of width, the risk-reward is structurally unfavorable.

A key rule for iron condors is to position the wings far out.