Most options traders spend their careers focused on directional trades, premium selling, and volatility plays. Few ever discover that buried inside the options market is a structure that delivers a completely guaranteed return – one that doesn’t care whether the market goes up, down, or sideways, and that Wall Street institutions have been using quietly as a financing tool for decades.

That structure is the box spread. And with interest rates running at their highest levels in years, it’s worth understanding precisely.

A box spread combines two vertical spreads: a call spread and a put spread, across the same two strike prices and the same expiration. The payoff at expiration depends on the strike width, no matter where the underlying trades. It doesn’t matter if the S&P 500 rallies 30% or crashes 40%. At expiration, the box pays exactly what the arithmetic dictates. No directional risk. No volatility risk.

When used right on European-style index options, it acts like a lending tool. It can collect near T-bill rates, offering good tax benefits. Also, it’s one of the cheapest borrowing options for savvy retail traders. Hedge funds, family offices, and prop shops have been using box spreads as a financing mechanism for decades. In 2024, average daily notional volume on SPX box spreads exceeded $900 million, according to the CBOE. This is institutional infrastructure that retail traders now have access to.

Here is everything you need to know to use it.

What Is a Box Spread?

The box spread consists of four options legs across the same two strike prices and the same expiration date:

- Buy the lower strike call

- Sell the upper strike call

- Buy the upper strike put

- Sell the lower strike put

The call spread and put spread offset each other in a way that eliminates all directional exposure. At expiration, the combined position is worth exactly the difference between the two strike prices. Always, without exception. If your strikes are 100 points apart on SPX, the position settles to $10,000 at expiration regardless of where the index finishes.

Because the terminal payoff is fixed, the only question is what you pay or receive today versus what you collect or owe at expiration. That gap implies an interest rate. This is what makes the box spread so elegant – it is a fixed-income instrument built entirely from options, priced by the same forces that set Treasury yields.

A long box spread costs money today and pays out a larger fixed amount at expiration. You are lending money to the options market at the prevailing rate.

A short box spread receives money today and pays out a larger fixed amount at expiration. You are borrowing money from the options market, often at rates well below what any broker charges for margin.

The Box Rate: What Researchers Found

Researchers at the New York Fed have studied what they call the “box rate” – the risk-free interest rate implied by S&P 500 index options through put-call parity. In a 2023 Liberty Street Economics post, they showed box rates can be estimated very precisely. The R-squared of the put-call parity regression is .99999992, reaching up to seven nines. Its standard error is below one basis point.

What this means practically: the options market is pricing risk-free rates with near-perfect accuracy. The box rate closely tracks (but sits slightly above) equivalent-maturity Treasury yields. The spread between box rates and Treasury yields, which the Fed researchers call the convenience yield, historically runs 10 to 30 basis points across different maturities. Treasuries trade below box rates because they are the ultimate safe asset. Investors demand them not only for their yield but also for their liquidity and their role as collateral in the global financial system.

For traders, this framing is more powerful than the “free money” narrative that sometimes surrounds box spreads. You are not exploiting a loophole, you are accessing the options market’s funding curve – a market where put-call parity turns options into a precise financing instrument, and where the clearing of that market through the OCC prices borrowing and lending with institutional accuracy.

The One Rule You Cannot Break

Before going further, one rule must be stated clearly: box spreads only deliver a fixed terminal payoff with European-style options, which can only be exercised at expiration, not before. SPX options are European-style and cash-settled. This eliminates early assignment risk entirely. The position behaves exactly as the math predicts, right through to expiration.

American-style options on individual stocks, SPY, QQQ, most equity ETFs, carry early assignment risk. Your short legs can be exercised against you at any point before expiration, even when it appears irrational to do so. When that happens on a large position, the symmetry of the box collapses. The four legs stop offsetting each other, and the results can be severe. Use SPX.

A Real Long Box Example on SPX

With the S&P 500 at 5,600, here is a concrete long box spread using one-year expirations:

| Leg | Strike | Action | Cost |

|---|---|---|---|

| Call | 5,550 | Buy | $488.95 |

| Call | 5,650 | Sell | ($422.45) |

| Put | 5,650 | Buy | $248.65 |

| Put | 5,550 | Sell | ($219.95) |

| Net cost | $95.20 |

The spread between strikes is 100 points. With SPX’s $100 multiplier, the fixed payoff at expiration is $10,000 per contract, regardless of where the index settles. Total invested: $9,520 ($95.20 × 100). Fixed payoff at expiration: $10,000. Your profit: $480. Implied annual return: 5.04% (480 / 9,520).

That 5.04% is the rate the market is paying you to lend it money for one year, aligned with prevailing risk-free rates. There is no directional risk at expiration, however before expiration, the market value of the box can fluctuate with interest rates, liquidity conditions, and marking conventions. The OCC, not the U.S. government, stands behind performance. Schwab has explicitly flagged execution risk, marking considerations, and collateral requirements as real-world factors traders must account for.

Two things are essential in execution. First, place the entire four-leg position as a single order; never leg into a box spread one option at a time, because you carry directional risk between fills. Second, account for bid-ask spreads and commissions. The numbers above assume mid-market fills. In practice, your fills will be slightly worse on each leg, which is why this strategy only makes economic sense at meaningful contract size.

You can adjust the size and maturity of a box spread by choosing different strike widths and expiration dates. A wider strike spread results in a larger notional amount. A longer expiration means a longer duration for the lending or borrowing, and more total premium, though the annualized rate stays anchored to prevailing interest rates.

Box Spreads as Cheap Loans

The same structure in reverse is where the strategy becomes especially powerful for sophisticated traders who need liquidity without selling positions.

A short box spread receives a net credit today and delivers the fixed spread value at expiration. You are effectively borrowing money from the options market at the box rate, which runs 30 to 50 basis points above equivalent-maturity Treasury yields, and far below what any broker charges for margin.

The comparison to margin is stark. Margin loan rates at major brokerages frequently exceed 10% annually. A box spread loan on SPX using one-year options has recently priced in the 4.5% to 5% range. For a trader with a large, low-cost-basis portfolio who needs liquidity without triggering a taxable sale, the savings over the life of a multi-year loan can be substantial.

In 2024, the average daily notional volume on SPX box spreads exceeded $900 million, according to CBOE, driven largely by institutional participants using them as exactly this kind of financing tool. Cboe’s own analysis has noted that box spread borrowing rates are often comparable to – and in some environments, better than – Treasury yields or margin loans, while flagging that short boxes carry collateral and margin risk that traders must manage actively.

To execute: sell the short box spread, receive the net credit today, and at expiration deliver the larger fixed amount. Your rate locks at execution and cannot be recalled early. There are no margin calls during the life of the trade driven by the options position itself, though your broker may impose their own collateral requirements. The term is fixed to your chosen expiration.

An Alternative to Treasury Bills?

A long box spread functions like a zero-coupon instrument. You pay a known amount today, receive a larger fixed amount at expiration, and the difference is your return. The comparison to T-bills is direct and favorable.

Box spreads priced through the options market have historically offered returns modestly above equivalent-maturity Treasuries, reflecting the convenience yield that Treasuries carry as the ultimate safe collateral asset. The New York Fed’s research shows this spread running 10 to 30 basis points historically, though it varies with market conditions. Whether that advantage materializes in practice depends on execution quality, commissions, and whether you hold to expiration.

The tax picture is more nuanced than often presented. Certain cash-settled index options including SPX may qualify for Section 1256 treatment, which applies a blended 60/40 rate: 60% taxed at long-term capital gains rates and 40% at short-term rates, regardless of holding period. At the highest federal rates, this implies an effective federal rate of approximately 26.8% versus 37% for ordinary income.

On a 5% pre-tax yield, that difference translates to roughly 0.5 percentage points of additional after-tax return. Meaningful, but not dramatic. The IRS has noted that some box spread structures could be reclassified. The tax outcome varies based on how the positions are set up and reported. Consult a tax advisor before treating the Section 1256 benefit as automatic.

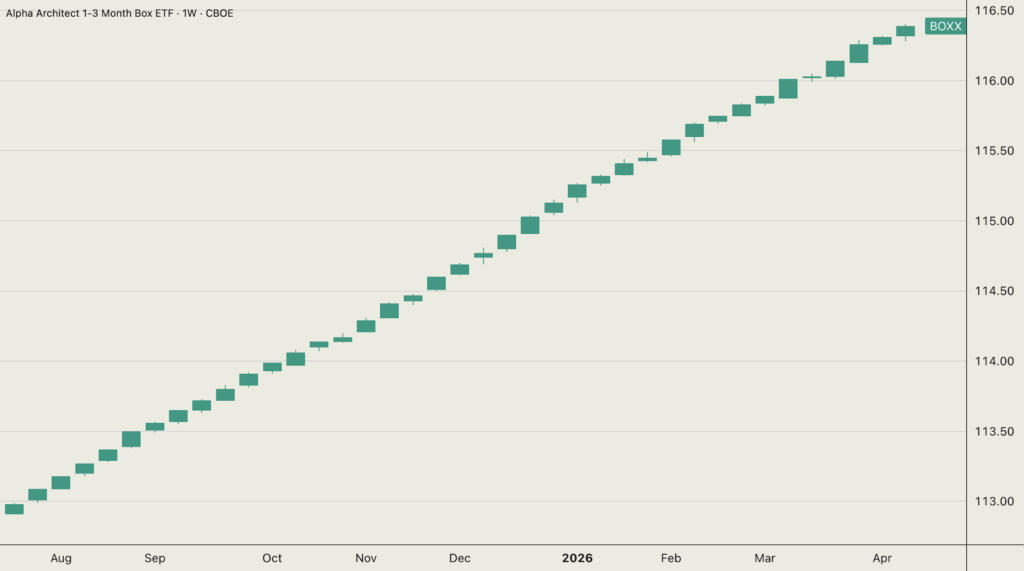

BOXX: The One-Click Retail Wrapper

BOXX – the Alpha Architect 1-3 Month Box ETF – is the closest retail approximation of box spread economics in an ETF wrapper. Launched in December 2022, the fund had grown to over $8 billion in AUM by late 2025, attracting $4.1 billion in inflows that year alone. The concept is elegant: roll 1-3 month box spreads systematically, target T-bill equivalent returns, and deliver the result in an ETF structure that aims for capital gains treatment rather than ordinary income distributions.

BOXX is important to know about, but it needs careful description. It isn’t a guaranteed better option than trading SPX boxes directly. Its tax treatment, distribution behavior, and holdings mix can differ from a direct SPX box position. BOXX made a taxable distribution in 2024, and the current prospectus explicitly states there is no guarantee the fund will avoid distributions. The fund also retains flexibility to use options on ETFs other than SPX when those offer better characteristics, meaning the holdings may not always be pure European-style index options. The expense ratio is 0.19%.

For traders who want box spread economics without executing four-leg orders, BOXX is the practical starting point. For traders at meaningful scale who want to control terms, expiration, and avoid the management fee, executing SPX box spreads directly remains the more precise approach.

Alternatives to Box Spreads

U.S. Treasury bills are the direct equivalent, backed by the federal government, available through TreasuryDirect or your brokerage, no options approval required. The yield is slightly lower and the tax treatment is ordinary income, but the execution is as simple as it gets.

BIL (SPDR Bloomberg 1-3 Month T-Bill ETF) and SHV (iShares Short Treasury Bond ETF) offer straightforward T-bill exposure with daily liquidity. Returns are taxed as ordinary income. This is the main downside compared to box spread strategies.

IBKR’s cash yield program automatically earns interest on uninvested cash at competitive rates. Zero complexity, no options approval required. IBKR is also the most capable retail platform for executing actual box spreads when you are ready to trade the strategy directly.

The advantage of doing it yourself – executing box spreads directly on SPX – over BOXX is customization: you control the expiration, the notional size, and you avoid the management fee. At meaningful scale, that fee compounds. At smaller account sizes, BOXX is simply easier and still delivers the core economic benefit.

The Bottom Line

A box spread on European-style index options is as close to risk-free as options trading gets. The payoff comes from arithmetic, not market direction, creditworthiness, or implied volatility. Used correctly – as a single order, with a clear understanding of the execution, marking, collateral, and tax realities – it is a genuine institutional-grade tool for lending, borrowing, and cash management that the professional world has used for decades while most retail traders have never heard of it.

As a lender, it can price slightly above T-bills based on execution and market conditions, while qualified traders may benefit from favorable tax treatment under Section 1256. As a borrower, it frequently beats margin loans substantially. It’s a cash management tool that falls between T-bills and BOXX in complexity. It demands more work than either but gives you more control.

What makes it genuinely interesting is the mechanism: put-call parity turns the options market into a precise financing market, and the box spread is how you access it. The Fed researchers found the box rate tracks risk-free rates with seven-nines accuracy. The institutions figured out decades ago that this precision was useful. The only question is whether you are ready to use the same infrastructure.

The OptionsJive Trading Plan covers more creative ways to use options as both a trading and portfolio management tool – download it here to see how box spreads and short premium strategies fit together.

Great overview of box spread, but I love the story about Robinhood user, who tried to set up a box spread with just $5k in his account, he ended up facing a loss of over $60k after some options were exercised against him. It’s wild how this incident led to Robinhood banning box spreads altogether!