Imagine a bottle of water costs $1. You can buy it for $0.90, and someone paid you $0.10 just to wait for that price. You’re already ahead before you’ve done anything.

In the stock market, this is exactly how cash-secured puts work. You can get paid to buy any liquid stock or ETF you want, at a price below where it currently trades, collecting premium upfront just for committing to a purchase you already wanted to make. If the stock never reaches your price, you keep the money and try again. If it does, you own it cheaper than the day you started waiting.

Institutional investors and hedge funds use this quietly and systematically. So does Warren Buffett – he collected $7.5 million from Coca-Cola in 1993 without buying a single share. And any retail investor with a basic options account can run the exact same trade, including inside an IRA.

What a Cash-Secured Put Actually Is

When you sell a put option, you take on an obligation – if the option buyer chooses to exercise, you buy 100 shares of the underlying stock at the strike price. In exchange for accepting that obligation, you collect a premium upfront. That cash is yours immediately, regardless of what happens next.

The “cash-secured” part is what makes this conservative. You hold enough cash in your account to fund the full purchase if it comes. No margin, no leverage, just capital you’d already decided to spend on this stock, now sitting in a money market fund earning interest while it waits.

At expiration, two things can happen. Either the stock stays above your strike and the put expires worthless – you keep the premium and your cash is freed up – or the stock falls below your strike and you’re assigned, buying 100 shares at your target price. Your real cost basis is the strike minus the premium you already collected.

Both outcomes leave you better off than a simple limit order. The limit order pays you nothing while you wait. The cash-secured put always does.

The Buffett Trade

April 1993. Coca-Cola is trading around $39. Buffett already owns 93.5 million shares and wants more, but not at $39. He’s decided that $35 would be a price worth paying. Instead of placing a limit order and sitting on his hands, he does something more interesting.

He sells 50,000 put contracts, five million shares equivalent, at the $35 strike, expiring December 17, 1993. For agreeing to buy KO at $35 if asked, he collects $1.50 per share: $7.5 million in cash, received immediately. Berkshire sets aside the $175 million needed to cover the purchase. Fully secured, no leverage.

From there, only two things can happen. KO drops below $35 and he buys five million shares at an effective cost of $33.50, exactly the price he wanted. Or KO stays above $35, the puts expire worthless, and he pockets the $7.5 million and moves on.

KO never fell to $35. Buffett kept everything.

The lesson here isn’t that cash-secured puts always work out perfectly. It’s that Buffett ran the process in a specific order: he found a business he understood, decided on a price he considered fair, and only then sold the put to get paid while waiting. The premium was secondary. The stock was the point. That sequencing – stock first, income second – is what makes this strategy sound rather than reckless.

Why It Works for Conservative Investors

Most options strategies either carry undefined risk or require margin, which is why they don’t belong in retirement accounts. Cash-secured puts have neither problem.

The maximum loss is completely bounded. If you sell a $50 put and the company goes to zero, you lose $50 per share minus the premium – painful, but no worse than if you’d simply bought the stock at $50. You cannot lose more than you would have by owning the stock outright.

Because you hold the full purchase price in cash, no margin is involved. That’s why Fidelity, Schwab, tastytrade, and Interactive Brokers all permit cash-secured puts in IRA accounts. You typically need only Level 1 or Level 2 options approval. Naked puts, sold without cash backing, are a different instrument entirely and don’t qualify for IRA accounts. The cash-secured version exists specifically because full cash coverage removes the leverage risk that makes options dangerous in retirement accounts.

There’s also a mindset shift that matters. For an investor who already wants to own a stock at a lower price, assignment isn’t a bad outcome; it’s the trade working exactly as intended. You got the shares you wanted at the price you chose. When that realization settles in, the anxiety that most new options traders feel around assignment simply disappears.

Picking Your Strike

Everything here comes back to one question: at what price would you actually be happy owning this stock?

That’s your strike. Not where a chart shows support, not where the stock “should” find buyers. The price where you’d click buy without hesitation if your limit order filled there today. Buffett picked $35 for KO because he’d independently decided $35 was a fair price for a business he understood. If you wouldn’t be genuinely comfortable owning the stock at the strike even if it kept falling afterward, don’t sell that put.

For income-oriented trading, the practical range is the 16-to-30 delta zone; roughly 5 to 15% out of the money. At 16 delta, you have about an 84% chance of simply keeping the premium. At 30 delta, the premium is richer but assignment is more likely. Go much below 16 delta and the premium gets too thin relative to the capital you’re setting aside. Go near the money and you’re essentially saying you want the shares right now – which is fine, but that’s a different trade.

Picking Your Expiration

Thirty to 45 days to expiration is where theta decay does its most efficient work. The option sheds value fastest in this window, without forcing you to manage the gamma risk that builds in the final week before expiration. Monthly cycles on quality names is my natural rhythm.

Before entering any trade, run this calculation:

Annualized return = (premium ÷ strike) × (365 ÷ days to expiration) × 100

A 30-day put on a $180 stock paying $2.40; that’s ($2.40 ÷ $180) × (365 ÷ 30) × 100 = 16.2% annualized. Running this on every candidate keeps you from being seduced by dollar premiums that look large but are mediocre once you account for capital lockup and time.

Enter when implied volatility is elevated. Cash-secured puts are short vega; they benefit when IV contracts. When IVR is above 25 or 30, the premium on your target strike is fatter, your breakeven sits lower, and volatility’s natural tendency to mean-revert works in your favor as the trade ages. Selling puts into crushed, dead-low volatility means thin premium and almost no cushion. It’s the worst version of the trade.

A Real Example

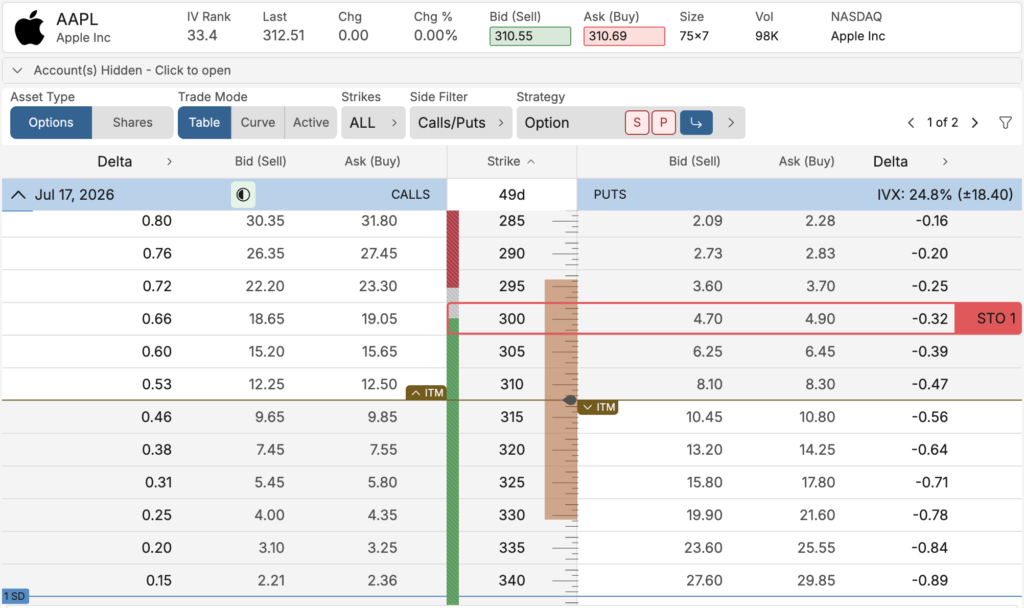

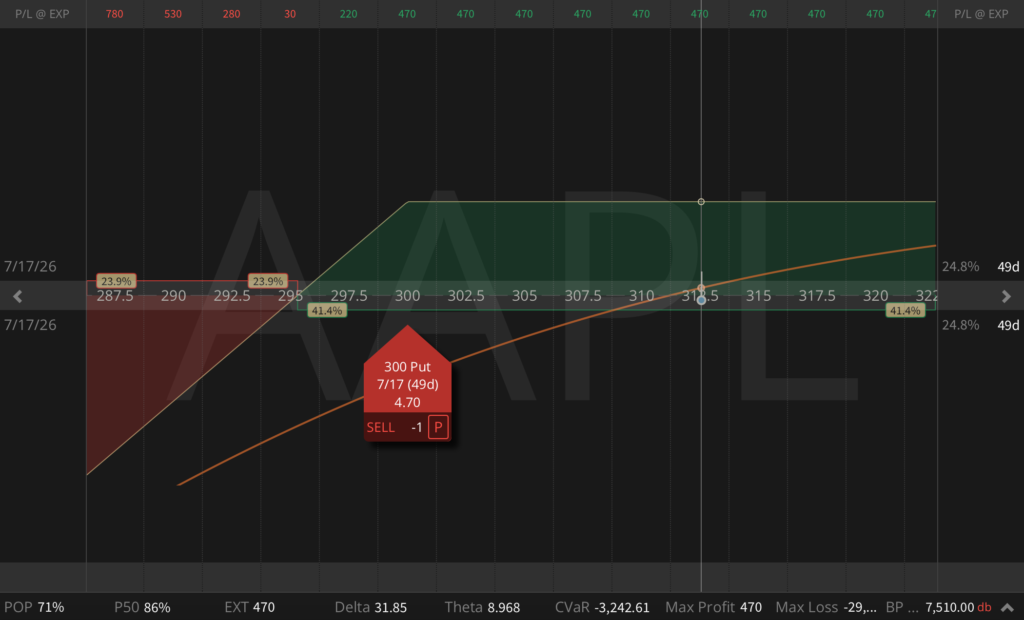

Apple is trading at $312. You’ve decided you’d be happy owning it at $300. IVR is 33. The 49-day $300 put is going for $4.80. You sell one contract and collect $480. You set aside $30,000 in cash.

Annualized return: ($4.80 ÷ $300) × (365 ÷ 49) × 100 = 11.9%. Not bad for money that was going to sit in a money market fund at 4%.

Three scenarios at expiration:

AAPL above $300: The put expires worthless. You keep $480. Sell another put next cycle. The capital never left your account.

AAPL at $295: You’re assigned at $300. Effective cost basis: $296.20 after the premium. You own a stock you wanted at a price that beats where it was when you started. You can immediately begin selling covered calls against the shares.

AAPL at $290: You’re assigned at $300, effective basis $296.20, while the stock trades at $290. This is where the real risk lives. The $4.80 premium gave you $4.80 of cushion. This scenario is exactly why the strike must be a price you’d own enthusiastically, not optimistically.

Managing the Trade

Cash-secured puts don’t require daily attention. But a few decisions come up regularly.

When you’ve captured about half the available premium, consider closing early. If you collected $4.80 and you can buy it back for $2.40, you’ve taken the bulk of the available theta. Holding for the last bit means carrying gamma risk for diminishing reward. Take the profit, free the capital, and put it to work again.

If the stock drifts toward your strike and you’d rather not take assignment yet, you roll down and out. Here’s what that looks like with actual numbers.

Say you sold a 30-day $50 put for $0.90 with the stock at $51. Now the stock is at $48.50 with expiration close, and that put is trading at $1.55. Buying it back alone locks in a loss. So you don’t just buy it back. In one order, you buy to close the $50 put and simultaneously sell a $47.50 put 90 days out, which is trading at $1.70. Net credit on the roll: $0.15. You’ve lowered your obligation by $2.50 a share, bought yourself three more months, and still collected premium to do it.

When to Roll, and When to Accept

There’s a subtler version of that decision worth knowing. When your put goes in-the-money and IVR is high, say 65, the premium on that put is still inflated by both elevated volatility and the structural put skew that exists in equity markets. Rolling for a credit in that environment is often more profitable than accepting assignment and switching to covered calls, because you keep harvesting that rich premium. The instinct is to take the shares and move on. The better move, when IV is elevated, is frequently to keep rolling and keep collecting while the skew is paying you to wait.

And sometimes the right move is just to let assignment happen. If the stock closes below your strike and your thesis is intact – the business is fine, the decline is macro-driven, the valuation is better now than before – you own the stock you wanted at the price you chose. Selling covered calls against it from there is the natural continuation.

If the thesis has changed – a real problem inside the business, a sector unraveling, something that makes you genuinely not want to own this company anymore – buy the put back and take the loss cleanly. The ability to recognize the difference between a temporary dip and a changed story is worth more than any rolling rule.

Early Assignment

New put sellers worry about early assignment more than they should. Technically, US options are American-style and can be assigned any time before expiration. In practice, early assignment on a cash-secured put is rare, and when it happens, it’s usually fine, because you wanted the stock anyway.

Early assignment becomes rational for the put holder only when the option is deep in-the-money with nearly no extrinsic value remaining. At that point there’s no reason to wait, so they exercise. But for a cash-secured put seller, that just means buying the stock a few days early.

The one genuine exception: corporate events. A merger, takeover, spin-off, or special dividend can completely disrupt normal assignment behavior. If a stock you’ve sold puts on announces something material, check the position and don’t assume the usual logic applies.

Cash-Secured Puts vs. Limit Orders

Most investors who’d benefit from this strategy are already doing the equivalent in a worse way: placing limit orders.

A limit order to buy AAPL at $180 locks up $18,000, generates zero income while you wait, and either fills or doesn’t. The cash-secured put does the same thing – reserves $18,000, potentially buys AAPL at $180 – but pays you $240 for committing to it. Same stock-acquisition outcome. One pays you. One doesn’t.

The one real difference: a limit order can fill anywhere down to $180, so if AAPL craters to $140 on earnings, you’re already in at $180. The cash-secured put assigns you at $180 regardless of how far below that the stock goes. If catching an exact bottom is the goal, a limit order’s flexibility is genuinely useful. But if you have a fundamental conviction on a quality business and you’re comfortable owning it through volatility, which is the only situation where you should be selling these puts, the cash-secured put is the limit order that pays you.

Cash-Secured Puts for European Investors

There is one additional application of cash-secured puts that almost no guide mentions, and it is particularly relevant for European investors.

Under EU PRIIPs regulations, most brokers block European retail clients from directly purchasing US-domiciled ETFs like SPY, QQQ, IWM, or TLT. The reason is straightforward: US ETF issuers generally don’t provide the Key Information Document required under European rules, so the direct purchase route is closed off for retail accounts.

Options, however, create a different path. Many European brokers still allow options trading on those same US ETFs. That means a cash-secured put can become a practical acquisition tool: you sell a put on the ETF you want to own, fully reserve the cash, and if assigned, you receive the shares through assignment rather than a direct purchase order. You are not buying the ETF, you are fulfilling an options obligation.

This is not a shortcut to use carelessly. It comes with broker-specific rules, tax implications, US estate tax considerations for non-resident holders of US assets, and currency exposure. Interactive Brokers explicitly notes that EEA and UK retail clients generally cannot purchase US-listed ETFs without a KID, though options remain available in many accounts. Before using this approach, verify the rules with your specific broker and consider the tax treatment in your jurisdiction.

For sophisticated European investors who understand options mechanics and genuinely want systematic exposure to US-domiciled ETFs, cash-secured puts can be more than an income strategy. They become a practical acquisition route through options assignment, working within broker rules rather than around them.

The Wheel: The Natural Next Step

Cash-secured puts don’t have to be a standalone strategy. They are also the entry phase of one of the most popular systematic income approaches in options trading: the Wheel.

You sell cash-secured puts on a stock or ETF you’d be happy to own. If the put expires worthless, you keep the premium and sell another one next cycle. If you’re assigned, you now own 100 shares at your chosen strike, with your cost basis already reduced by every premium you’ve collected along the way. From there, you sell covered calls against the shares, getting paid again while you hold them. If the stock rallies through your call strike, the shares get called away at a profit and you return to selling puts. Then you repeat the whole cycle.

That’s the Wheel. Sell puts until assigned. Sell covered calls until called away. Restart.

It turns stock ownership into a repeatable premium-harvesting process; you collect income at entry, income while holding, and potentially a capital gain on exit. The cash-secured put is what gets you paid to wait for the right price. The covered call is what gets you paid while you own it.

The Wheel is not magic, and it carries the same fundamental requirement as every cash-secured put: you need to genuinely want to own the underlying. Use it on high-quality stocks and ETFs you’d hold anyway, size it so assignment is always manageable, and avoid chasing premium in broken names. Done correctly, it’s one of the cleanest ways to combine a value investor’s discipline with systematic options income.

Why Puts Pay More Than Covered Calls

In equity markets, puts carry higher implied volatility than equivalent-delta calls; the persistent put skew that exists because institutional demand for downside protection is permanently elevated. Someone is always buying portfolio insurance.

That skew lands in your pocket. At equivalent deltas, a cash-secured put typically collects 5 to 15% more premium than a covered call in neutral-to-bearish conditions. You’re being paid extra for selling exactly what institutional buyers always need. In strongly bullish momentum names, call skew can briefly reverse this, but most of the time, on most quality underlyings, the put side is richer. It’s the same edge the jade lizard is built around.

The Risk Nobody Warns You About

Assignment isn’t the risk. The real risk is selling puts on the wrong stocks.

The traders who get hurt are the ones who go shopping for premium rather than for companies. They find a volatile, cyclical, or fundamentally troubled name with a fat implied volatility, sell the put because the income looks attractive, and then get assigned into a business they never actually wanted to hold through a prolonged decline. The premium looked like free money, but the stock position looked like a disaster.

Buffett’s discipline was to run the process in the opposite order. He found businesses he had deep conviction in, independently decided on prices he considered fair, and only then sold puts to get paid while waiting. The premium wasn’t the point. It was a side effect of having a clear view on a quality company at a compelling price. Get that sequence backwards and the strategy quietly becomes a machine for accumulating your worst ideas.

The single filter that prevents this: before selling any put, ask yourself whether you would buy the stock outright at the strike price today, with full knowledge that it might keep falling. If the honest answer is yes, sell the put. If there’s any hesitation, don’t.

Is This Right for You?

If you’re a value investor who keeps target prices on quality companies and currently expresses them through limit orders, this strategy is strictly better. You’d collect income instead of nothing while you wait.

Cash earmarked for future stock purchases but sitting in a money market at 4% can work harder through cash-secured puts, generating meaningfully higher yields on capital you were already planning to deploy.

If you trade inside an IRA and want options exposure within the account’s constraints, this is one of the very few strategies consistently permitted across brokerages.

If undefined risk keeps you up at night, the bounded downside here – never worse than owning the stock outright – is about as conservative as options selling gets.

The strategy is the wrong tool when premium-hunting overrides stock-quality discipline. And it’s the wrong tool when you can’t genuinely afford to own the stock at the strike; if a $5,000 assignment would strain the account, the position is too large.

The OptionsJive Trading Plan covers puts as part of a broader short premium framework; how to select underlyings, size positions, manage assignments, and transition into covered calls once shares are acquired.

Frequently Asked Questions

What is a cash-secured put?

Selling a put option on a stock you want to own while holding enough cash to buy the shares at the strike price if assigned. You collect premium upfront and either keep it when the stock stays above the strike, or buy the stock at your chosen price when it falls below.

Are cash-secured puts allowed in an IRA?

Yes. Most US brokerages permit them in IRAs because they require no margin and maximum loss is fully defined. Fidelity, Schwab, tastytrade, and IBKR all allow them with Level 1 or Level 2 options approval.

What is the maximum loss?

The strike price minus the premium collected, times 100 – realized only if the stock goes to zero. Identical to the downside of simply buying the stock outright.

How do I calculate the annualized return?

(Premium ÷ strike) × (365 ÷ days to expiration) × 100. This lets you compare trades across different expirations on equal footing.

What strike should I choose?

The price at which you’d genuinely be happy owning the stock. Practically, the 16-to-30 delta range (5-15% out of the money) balances income against probability of assignment.

What expiration should I use?

30-45 days for income generation. Close at roughly 50% of max profit rather than holding to expiration.

What happens if I’m assigned?

You buy 100 shares per contract at the strike, funded by reserved cash, at an effective cost of strike minus premium. For a cash-secured put seller this is a normal outcome; you’ve acquired a stock you chose at a price you chose.

Can European investors use cash-secured puts to acquire US ETFs?

In some cases, yes. Many European retail investors cannot directly buy US-domiciled ETFs because issuers don’t provide the PRIIPs Key Information Document. However, some brokers still allow options trading on those ETFs, and assignment from a cash-secured put may result in receiving the shares.

How does a cash-secured put fit into the Wheel strategy?

A cash-secured put is the entry phase of the Wheel. You sell puts until assigned, at which point you own the shares at your target price. You then sell covered calls against those shares. If called away, you return to selling puts and repeat the cycle, collecting premium at every stage.

Why do cash-secured puts often pay more than covered calls?

Put skew. Equity puts carry higher implied volatility than equivalent-delta calls because institutional demand for downside protection is structurally elevated. At equal deltas, selling the put typically collects 5-15% more premium in most conditions.

Did Warren Buffett really use this?

Yes. In April 1993 he sold 50,000 KO put contracts at the $35 strike, collecting $7.5 million in premium when KO traded near $39. The options expired worthless in December 1993 and Berkshire kept everything. He used similar trades on multiple other positions over the years.